APYX Tokenomics: How the Governance Token Accrues Value

Token Structure, Float, and Reserve Growth

Apyx is live. Total value locked (TVL) just crossed $16 million and is growing like a weed, so it’s time to answer the question everyone is asking: what is APYX?

APYX is the future governance of the Apyx protocol, the first dividend-backed stablecoin (DBS) built on preferred equity yield from Digital Asset Treasuries (“DATs”).

This blog post covers APYX’s tokenomics, with emphasis on:

- (1) token allocation and float

- (2) how APYX accrues value, and how protocol fees flow to governance token holders

Token Supply & Float

APYX has a fixed supply of 100,000,000 APYX. There is no emissions schedule, no future minting, and no inflationary mechanism. The allocation is as follows:

All locked or vesting tokens follow a structured unlock schedule. To ensure incentives are aligned, core team tokens vest over 4 years. The full unlock schedule will be published before the token generation event (TGE) of APYX.

There are two things to note:

First, there are no venture capitalists (VC) to dump on users. This decision was deliberate. Too often, early VC investors get preferential treatment at the expense of the protocol’s community. APYX was funded by early contributors, strategic partners, and a handful of angel investors. There is no Series A investor sitting on discounted tokens waiting for a lockup to expire. This implies no token overhang. The people holding APYX at launch are the team that built it and the public that buys it.

Second, the float is tight, which means only a small percentage of the token supply is freely tradeable at launch. Most tokens are locked in multi-year vesting schedules and won’t hit the market anytime soon. Why does this matter? Fewer tokens in circulation means less sell pressure overhanging the market. Furthermore, because the foundation cannot earn staking rewards on their allocation, 100% of rewards goes to community members, core team and early investors mentioned above. This was a deliberate choice, not a side effect of the vesting schedule.

The APYX DAT

The team behind Apyx also built DeFi Development Corp. (Nasdaq: DFDV), the first non-bitcoin Digital Asset Treasury (DAT). A well-run DAT is an efficient vehicle for accumulating a digital asset over time. APYX is a strong candidate for a DAT of its own. A publicly-traded vehicle that holds APYX in its treasury would create consistent bid pressure for the token over time.

How APYX Accrues Value; Fee Switch *ON*

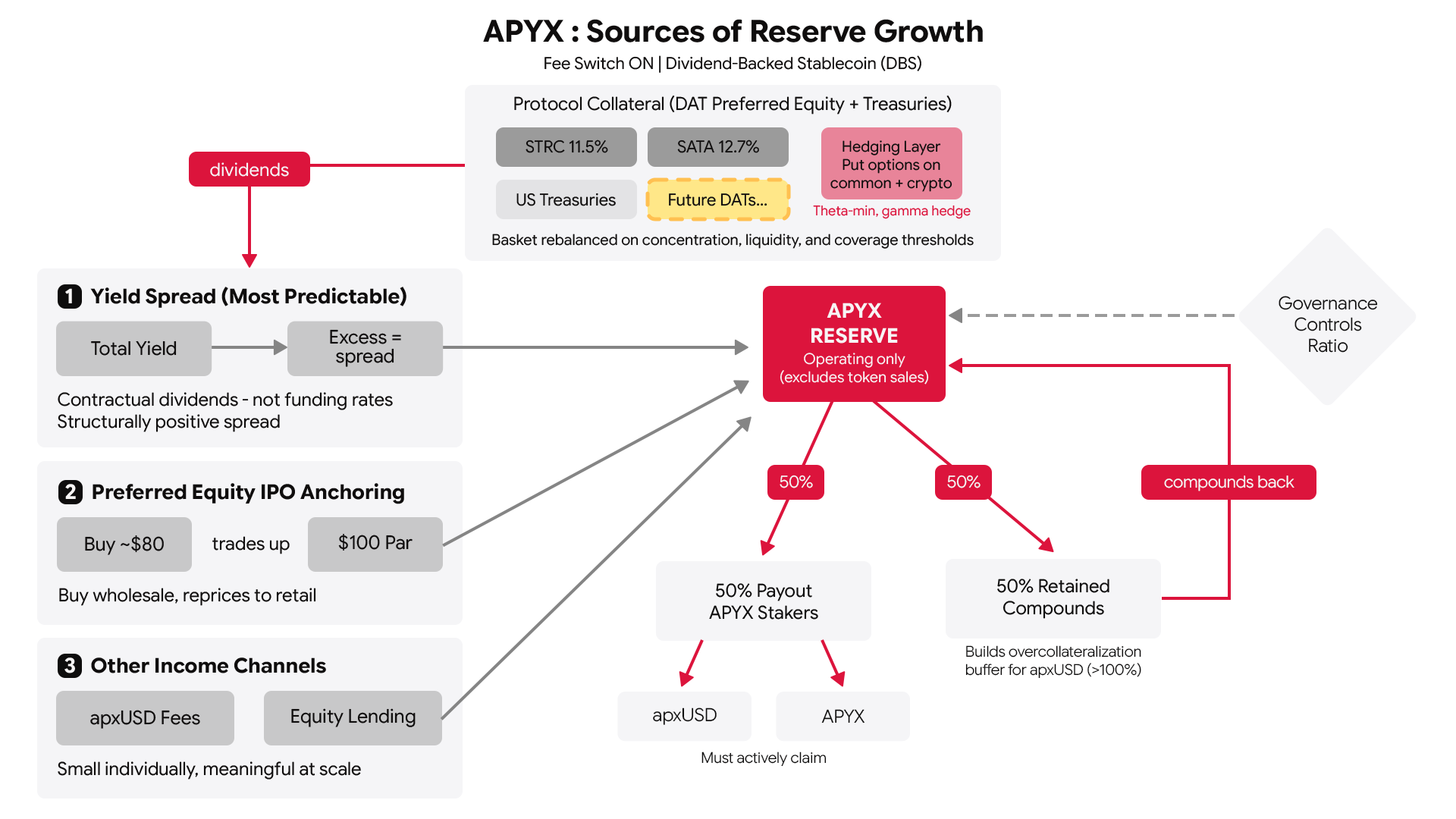

APYX value accrual is driven by reserve growth. The reserve is everything the protocol owns. It grows from three sources:

- 1. The spread between what the collateral earns, and what Apyx pays to apyUSD holders

- 2. Gains from preferred equity IPO participation, where preferred equity offerings typically price around $80 and trade up towards $100 par value shortly after, letting Apyx pocket the difference

- 3. Other sources of income, as described below

Excluded is growth from token sales, such as foundation APYX dispositions, from this definition. Reserve growth reflects operations, not the Foundation and its affiliates’ capital markets activity.

At launch, 50% of monthly reserve growth is paid out to APYX stakers. The other 50% stays in the reserve, compounding the asset base and building the overcollateralization buffer that protects apxUSD holders.

Stakers choose whether they receive payouts in apxUSD (dollar-denominated) or in additional APYX. In either case, rewards must be actively claimed. The 50% payout ratio is a starting point, subject to change by governance vote. As the overcollateralization buffer grows, governance could increase the payout, making it more attractive to hold APYX. This is a feature APYX holders control.

Sources of Reserve Growth

Reserve growth comes from three primary sources:

Collateral-apyUSD Yield Spread

The protocol holds DAT preferred equity and U.S. treasuries. Currently, the preferred equity held includes Strategy’s STRC (11.5%) and Strive’s SATA (12.7%). The yield generated from these preferreds, as well as U.S. treasuries, is used to payout apyUSD holders, with a targeted double-digit yield greater than that offered by any of the preferred equity held by the protocol. Excess yield is allocated to the protocol’s reserve.

- Reminder: When market participants mint apxUSD, the USDC the protocol receives may then be used to purchase preferred equity that backs apxUSD. However, to earn a yield, users must swap apxUSD for apyUSD. Market participants who opt to hold apxUSD instead of apyUSD enable apyUSD holders to earn higher yields than they would otherwise earn by holding the same preferred equity directly in their brokerage account.

This is the protocol's most predictable income source. Preferred dividends are structural obligations. The issuing DATs owe them regardless of what crypto markets are doing. This is not a funding rate that flips negative, or a basis trade that compresses in a downturn. Apyx is designed to provide stable payments even during adverse crypto market conditions. The collateral earns more than Apyx pays to apyUSD holders, and the spread is structurally positive.

Preferred Equity IPO Anchoring

When a DAT issues new preferred stock, it typically prices at a discount to par. For example, a new preferred stock might IPO at $80 on a $100 par instrument. Apyx intends to opportunistically participate in some of these new issuances as a buyer, acquiring preferred equity at this discounted IPO price. When the instrument trades up to par (which is the norm, not the exception), the protocol captures that spread. Think of it as buying at wholesale and holding an asset that reprices to retail.

Other Reserve Growth Mechanisms

The reserve also grows through smaller but steady channels: issuance and redemption fees on apxUSD, lending the preferred positions to borrowers through brokerage accounts, and other activities. None of these is large on its own. Together they add a meaningful layer of income, especially at scale.

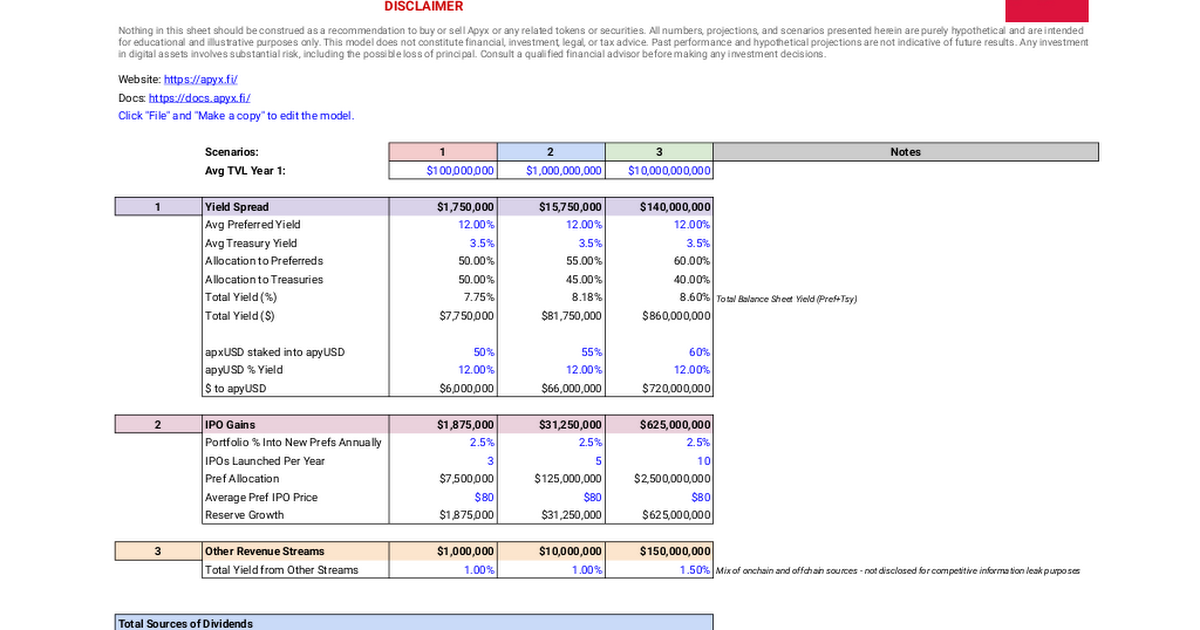

Valuation Modeling

Below is a spreadsheet to make it easier to build a own valuation model for APYX. Please review each variable and come to your own conclusions. If unsure, get your favorite AI tool to help.

Conclusion

APYX gives holders real cash flow from day one. Half of the protocol’s monthly reserve growth goes directly to APYX stakers. The other half compounds into a growing asset base that makes the protocol more durable over time.

The governance power is not ceremonial. It’s real economic value that accrues to holders. APYX controls how the reserve is allocated across preferred instruments. Real cash flow. Structural Growth. No venture overhang. That combination doesn’t exist anywhere else in DeFi. Starting day one, it belongs to APYX holders.