How STRC Became The Apex Digital Credit

A new asset class is emerging at the intersection of Bitcoin and traditional credit markets: Digital Credit. At the center of this development sits STRC, a preferred security issued by Strategy that is rapidly becoming the apex form of digital credit backed by the ultimate apex asset: BTC.

What makes STRC notable is not simply its yield, but the combination of structural protections, issuer incentives, and substantial collateral coverage that support it. Since launching in July 2025, STRC has demonstrated remarkable resilience, even during one of crypto’s most volatile stretches in recent memory. Over that period, its yield expanded from 9% to 11.5%, while Strategy repeatedly adjusted dividends to maintain price stability around par and continued accumulating Bitcoin with roughly $54B in BTC backing $10B in preferred notional.

Momentum is accelerating. During the week of March 9 alone, record STRC issuance funded the purchase of more than 20,000 BTC. STRC is not just another preferred security. It represents a new financial primitive, one that converts Bitcoin-backed balance sheets into income-producing instruments for global capital markets.

In this report, we explain how preferred equity works, why Strategy pivoted toward it as a financing tool, how STRC behaves in the market, how it compares to other instruments in the emerging Digital Credit stack, and what risks investors should consider.

The Unfamiliar Layer of the Capital Stack

Everyone has heard of debt and equity, but few have heard of what falls in between. In a corporate capital stack, the hierarchy from most senior to most junior runs: secured debt, unsecured or convertible debt, preferred equity, and finally common equity. In the event of liquidation, each layer must be made whole before the layer below it receives any proceeds. Preferred holders get paid after all debt holders are covered, but before any equity holders receive anything.

For investors, preferred equity offers a blend of characteristics from both sides of the capital structure. Like debt, it pays a stated dividend (analogous to a coupon) and has a par value (analogous to principal). Like equity, it is typically perpetual with no maturity date, dividends can be deferred or skipped without triggering default, and holders generally do not possess voting rights. This hybrid nature makes preferred equity particularly attractive for issuers seeking to raise capital without creating a hard maturity obligation and without diluting the voting control of common shareholders.

Not all preferred securities are created equal. The features that differentiate instruments within an issuer’s preferred stack include whether dividends are cumulative or non-cumulative (do missed dividends accrue as a liability, or are they permanently forfeited?), whether the rate is fixed or variable (is the coupon locked in at issuance or actively managed?), whether the security can be converted into common equity, and where the instrument sits within the preferred capital hierarchy. These structural differences determine the risk and return profile of each instrument and explain why two preferreds from the same issuer can behave very differently.

A cumulative preferred with a variable rate and senior positioning (like STRC) is structurally superior to a non-cumulative preferred with a fixed rate and junior positioning (like STRD). The former offers stronger protections across a wider range of scenarios. The latter compensates investors with a higher effective yield in exchange for accepting greater structural risk.

Strategy’s Strategic Pivot

The Convertible Playbook Ran Its Course

From 2020 through early 2025, Strategy’s primary means of raising debt was convertible senior notes, essentially loans from investors that can later be converted into the company’s stock under certain conditions. These instruments were particularly attractive because many carried little to no interest and had long maturities. In total, the company raised more than $8 billion, often paying 0% in cash interest, because investors were less interested in the coupon and more interested in the potential upside tied to the volatility of Strategy’s stock price.

However, convertible debt has an important limitation: it must eventually be repaid. Strategy’s convertible notes begin reaching key decision points starting in September 2027. If MSTR trades above the conversion price, investors convert into shares and the debt disappears. If the stock remains below the conversion threshold, Strategy must repay in cash. With $8.2 billion of these notes outstanding and MSTR currently trading around $130-$140, well below most conversion prices set when the stock traded above $300, a potential maturity wall emerges.

Preferred equity solves the maturity problem. Unlike debt, preferred securities are perpetual. There is no maturity wall, no put date, and no scenario in which preferred holders can force the company to repay principal. For a company whose balance sheet is largely concentrated in a single volatile asset, replacing maturing debt with perpetual preferred equity makes the company’s financial obligations far more stable and manageable

When Strategy’s Stock Premium Disappeared

For years, Strategy’s stock traded at a significant premium to its Bitcoin net asset value (mNAV). At its peak in November 2024, this premium reached 3.9x. This made issuing common stock extremely powerful: selling shares at 3-4x the Bitcoin backing per share and using the proceeds to buy more Bitcoin actually increased BTC per share for existing holders.

That premium has collapsed. As Bitcoin fell from its October 2025 peak near $126,000 to the mid-$60,000s in early 2026, MSTR dropped more than 70%, and mNAV fell below 1.0x. At an mNAV below 1, issuing common equity is mechanically dilutive to BTC per share. Preferred equity avoids this problem. STRC issuance raises capital for Bitcoin purchases without increasing the common share count. The cost is the dividend, not dilution. In a compressed mNAV environment, STRC has effectively become the primary engine for Bitcoin accumulation.

From Volatility Financing to Yield Financing

There is a deeper structural reason why STRC emerged when it did. Convertible debt thrives in a high-volatility environment because the embedded option to convert into equity is more valuable when the stock swings widely. When MSTR was moving 10-15% in a day, investors accepted 0% interest in exchange for that optionality.

But Bitcoin’s volatility profile has shifted. As the asset has matured, spot ETFs have launched, and institutional participation has deepened, realized volatility has compressed. Lower vol means the embedded option in convertible notes is worth less, making the terms worse for Strategy.

STRC represents a deliberate pivot to a low-volatility, high-leverage model. Rather than monetizing volatility through embedded options, Strategy is now monetizing its balance sheet through yield. STRC strips the volatility out of the Bitcoin position and sells the yield to income investors. The common equity (MSTR) absorbs the vol. The preferred equity (STRC) absorbs the yield. Strategy sits in the middle as a volatility refinery, separating a single asset into two distinct capital markets products for two different investor bases.

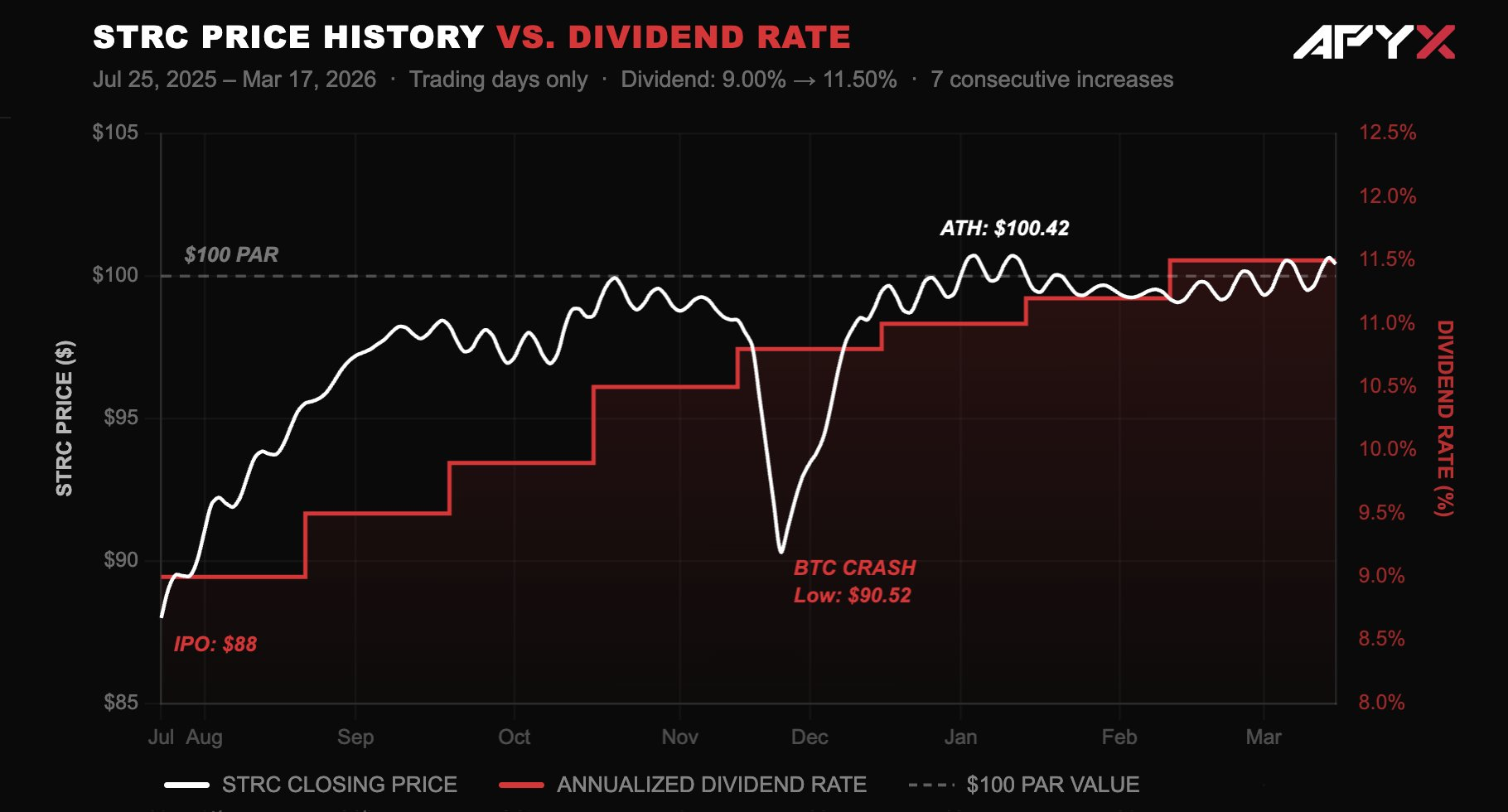

What STRC’s Price History Reveals

If STRC is functioning as designed, its price should remain relatively stable while the dividend adjusts to keep investor demand strong. The chart below shows exactly how that mechanism has played out since launch.

Looking back to August 2025, STRC has traded within an unusually tight range. Since the IPO, the security has traded between roughly $90.52 and $100.42, representing a range of about 10% over eight months. For comparison, in that same timeframe, MSTR traded between approximately $125 and $457 (a 265% range), and STRK moved between $71.40 and $129.48 (an 81% range). At 1.2% realized 30-day volatility (annualized), STRC exhibits the lowest volatility in the entire Digital Credit universe.

This stability is not accidental. The dividend rate functions as a built-in shock absorber. Each time STRC’s price drifted meaningfully below par, Strategy raised the dividend. Since launch, the rate has moved from 9.00% to 11.50% in a steady series of increases. After the November 2025 dip to $90.52, triggered by Bitcoin’s drop below $80,000, STRC recovered to near par within weeks as higher dividend rates restored demand.

The result is an instrument with a remarkably attractive yield-to-volatility profile. STRC delivers 11.50% annualized yield with very low price volatility relative to most income-producing assets. Traditional high-yield bonds at 7-8% carry meaningful credit spread and duration risk. Money market funds provide stability but yield 4-5%. STRC sits in a category of its own: double-digit yield, low volatility, monthly income, and tax-advantaged distributions.

Rethinking How Digital Credit Is Evaluated

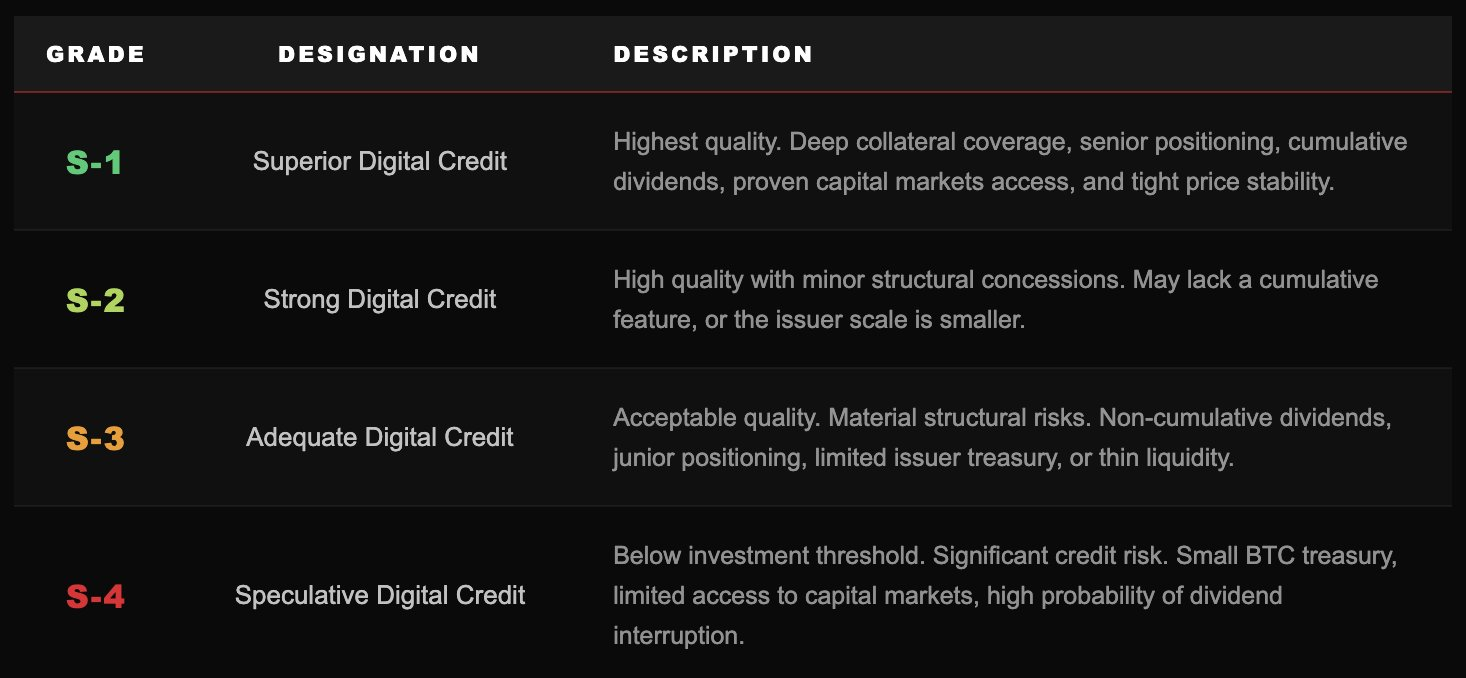

Traditional credit frameworks were designed for companies that generate operating cash flow to service debt. Bitcoin-backed preferred equity is different. Its strength depends less on EBITDA coverage and more on collateral backing, capital stack structure, issuer scale, and market liquidity. Applying traditional frameworks to Digital Credit instruments can be misleading. Rather than forcing these securities into boxes designed for corporate bonds, we developed the Satoshi Grade framework.

Under this framework, STRC earns an S-1, the highest grade. It ranks at the top across all five dimensions: more than 10x Bitcoin collateral coverage against STRC specifically, senior preferred positioning with cumulative dividends, a variable rate mechanism that actively stabilizes price, issued by the world’s largest Bitcoin treasury company, and deep trading liquidity averaging more than $200 million in daily volume in the last 30 days.

Why STRC Comes Out on Top

To understand why STRC ranks at the top, it helps to compare it against every other publicly traded Bitcoin-backed preferred security. The differences come down to structure.

The Variable Rate Advantage

STRC is the only Strategy preferred with a variable dividend rate. Rather than being fixed permanently at issuance, the dividend can be adjusted monthly to maintain price stability around par. This creates a self-correcting mechanism that fixed-rate instruments cannot replicate. STRK and STRD currently trade near $75, roughly a 25% discount to par, illustrating how fixed coupons expose investors to duration risk. STRC largely avoids that problem.

STRC vs. STRF: The Only Real Debate

STRF sits slightly higher in the preferred capital stack and pays a 10% fixed dividend with a ratchet that increases the rate if payments are missed. It also earns an S-1. However, STRC currently offers roughly 140 bps more in effective yield (11.55% vs 10.14%), pays monthly rather than quarterly, and has already proven its active price management mechanism through seven consecutive dividend increases. The trade-off: STRF ranks slightly higher and includes the dividend ratchet. Investors who prioritize absolute seniority over yield may prefer STRF.

STRK, STRD, and SATA: Higher Yield, Higher Risk

STRK’s conversion feature introduces equity correlation and 26% 30-day volatility. STRD carries the highest fixed coupon but sits lowest in the stack with non-cumulative dividends. SATA shares structural similarities with STRC, but is issued by Strive, a much smaller treasury company (~13,000 BTC vs. 760,000+). All three earn S-3.

Looking Under the Hood: The Issuer’s Balance Sheet

Structural protections tell only part of the story. Even the best-designed preferred security depends on the financial strength of the company issuing it. For Digital Credit instruments, what ultimately matters is how much hard collateral exists relative to the obligations sitting above preferred holders. The table below compares Strategy and Strive across metrics tailored to the Digital Credit framework.

Senior Debt / Hard Assets is the Digital Credit equivalent of a leverage ratio. Strategy’s 14.5% means for every dollar of BTC and cash, only 14.5 cents is owed to senior creditors. Hard Assets / Annual Obligations is the analog to interest coverage. Strategy’s 51.4x means its hard assets could theoretically cover 51 years of obligations. Cash / Annual Obligations measures near-term resilience: Strategy has 2.1 years of runway from cash alone, without selling any BTC or raising additional capital. BTC NAV / Preferred Notional measures the collateral cushion backing preferred equity specifically. Strategy’s 5.4x represents substantial overcollateralization.

Stress Testing the Model

How far would Bitcoin have to fall before the capital structure becomes stressed?

- BTC $71,000 (current): Hard assets cover total liabilities by 3.1x. Preferred covered over 5x. Comfortable.

- BTC $40,000 (-44%): Total liabilities still covered by 1.8x. Preferred backed by 3.3x. Cash reserve provides 2.1 years of runway regardless.

- BTC $25,000 (-65%): Liability coverage tightens to 1.2x but the structure remains solvent. Preferred still covered by 2.1x.

- BTC $15,000 (-80%): Total liabilities exceed hard assets. Even here, STRC sits ahead of billions in junior preferred and common equity. A principal loss requires BTC sustained at 2014-era levels long enough to exhaust cash reserves and prevent capital raises.

Dividend Sustainability: Can The Payments Last?

Strategy’s total annual preferred dividend obligation is approximately $1.1 billion. To support these payments, the company maintains roughly $2.25 billion in cash reserves, providing about 2.1 years of coverage even if no additional capital were raised. In practice, dividends are funded through capital markets activity. For context, in 2025 Strategy raised $25.3 billion in capital.

The key risk would be a scenario where Bitcoin enters a prolonged downturn while capital markets simultaneously close. Even then, the cash reserve provides years of runway. Strategy has navigated previous crypto winters without selling BTC or missing debt obligations. S&P Global assigned Strategy a B- credit rating with a stable outlook in October 2025, the first time a major agency rated a Bitcoin treasury company.

The Tax Advantage Most Investors Overlook

In 2025, all distributions from Strategy's preferred securities were classified as return of capital (ROC) for U.S. federal tax purposes. Management expects this treatment to continue for more than a decade.

ROC distributions are not taxed as ordinary income in the year received. Instead, they reduce the holder's cost basis in the shares, deferring the tax liability until the position is sold. At that point, the gain attributable to the reduced basis is taxed at the long-term capital gains rate (20% for top-bracket investors) rather than the ordinary income rate (37%). That 17-percentage-point spread makes a meaningful difference in after-tax yield relative to comparably yielding instruments like high-yield bonds, BDCs, or REITs, where distributions are typically taxed as ordinary income in the year received.

For investors who hold indefinitely, the deferral compounds. And in the case of an estate transfer, the cost basis steps up, potentially eliminating the deferred tax entirely.

The Risks

Even the strongest credit instruments come with risk, and Digital Credit is no exception.

- Bitcoin price volatility: Strategy’s ability to fund dividends depends on BTC value and continued capital markets access. A sustained decline below $30,000-$40,000 could pressure the financing flywheel.

- Dividend rate discretion: STRC’s rate can be adjusted by the company. While historically used to increase the dividend, the rate could theoretically be reduced to conserve capital.

- No direct BTC collateral: The Bitcoin treasury is not pledged as collateral. Preferred holders rely on overall balance sheet strength, behind $8.2 billion in senior convertible debt.

- Regulatory and legal risk: Multiple shareholder lawsuits filed. Changes to cryptocurrency regulation or tax treatment could impact operations.

- Capital stack complexity: There are five classes of preferred stock with $1.1 billion in annual dividends. The model depends on continued capital markets access.

Relative Value

STRC yields 450 bps above the broad high-yield index and offers yield slightly below CCC-rated credit, which currently yields around 13%. But this comparison flatters the CCC universe. CCC bonds carry substantial default risk, no collateral backing, and no mechanism to adjust coupons in response to market conditions. STRC offers cumulative dividend protection, more than 10x Bitcoin collateral coverage, active price management around par, and $2.25 billion in dedicated cash reserves.

When ROC tax treatment is factored in, the gap widens further. Because STRC distributions defer tax liability rather than generating ordinary income, the effective after-tax cash flow for top-bracket investors materially exceeds what a comparably yielding taxable instrument delivers. This combination of high-yield-tier income, low price volatility, tax efficiency, and substantial overcollateralization places STRC in a category that traditional fixed income instruments do not occupy.

The Next Financial Primitive

Digital Credit is still in its early stages, but the framework is taking shape. STRC is the first instrument to demonstrate that a Bitcoin-backed balance sheet can be reliably converted into a stable, yield-producing security at scale. That is a meaningful development for both Bitcoin capital markets and the broader fixed income landscape.

Among the emerging Digital Credit stack, STRC currently stands out. Its combination of structural protections, substantial Bitcoin backing, active dividend management, and deep market liquidity places it at the top of the category. As more issuers enter the space and the asset class matures, STRC will be the benchmark against which every future Digital Credit instrument is measured.

Important Disclosures

Satoshi Grade Methodology

The Satoshi Grade is a proprietary framework for evaluating Bitcoin-backed Digital Credit instruments. It is not affiliated with or comparable to ratings from Moody’s, S&P, Fitch, or any NRSRO. It reflects an independent assessment of relative credit quality within the Digital Credit asset class only and should not be used as the sole basis for any investment decision.

Disclaimer

This report is published by DeFi Development Corp. for informational and educational purposes only. It does not constitute investment advice, a recommendation, or a solicitation to buy, sell, or hold any security. The authors and/or DeFi Development Corp. may hold positions in the securities discussed. All information is believed accurate as of the date of publication but is not guaranteed. Investing in preferred equity, Digital Credit instruments, and Bitcoin-related securities involves significant risk including the potential loss of principal. Past performance is not indicative of future results.

This report is not a credit rating and should not be interpreted as one. The securities discussed are not FDIC insured, not bank deposits, and carry material risk of loss.