Introducing Apyx: Double-Digit Savings for Everyone

Introduction

Stablecoins represent the largest opportunity in all of crypto and are unequivocally the industry's first "killer app," yet they're fundamentally broken. Most offer limited transparency, limited alignment with holders, and virtually no native yield. Why should idle capital earn nothing while inflation steadily erodes purchasing power? Today, that all changes.

Introducing Apyx, the first Dividend-Backed Stablecoin (DBS) protocol backed by Digital Credit, alongside a globally accessible savings instrument built for double-digit yield at scale.

Simply put, apxUSD is a synthetic dollar backed by preferred equity issued by the most respected DATs, designed to channel high yield, offchain dividend cash flows into onchain dollar liquidity.

Apyx's savings asset, apyUSD, is the DBS that accrues enhanced yield from dividends paid by the DAT preferred shares backing apxUSD. It is designed as a scalable alternative to traditional stablecoin yield strategies that are often difficult to scale and rely on higher risk to generate returns.

The Unresolved Problems

The Trillion Dollar Yield Crisis

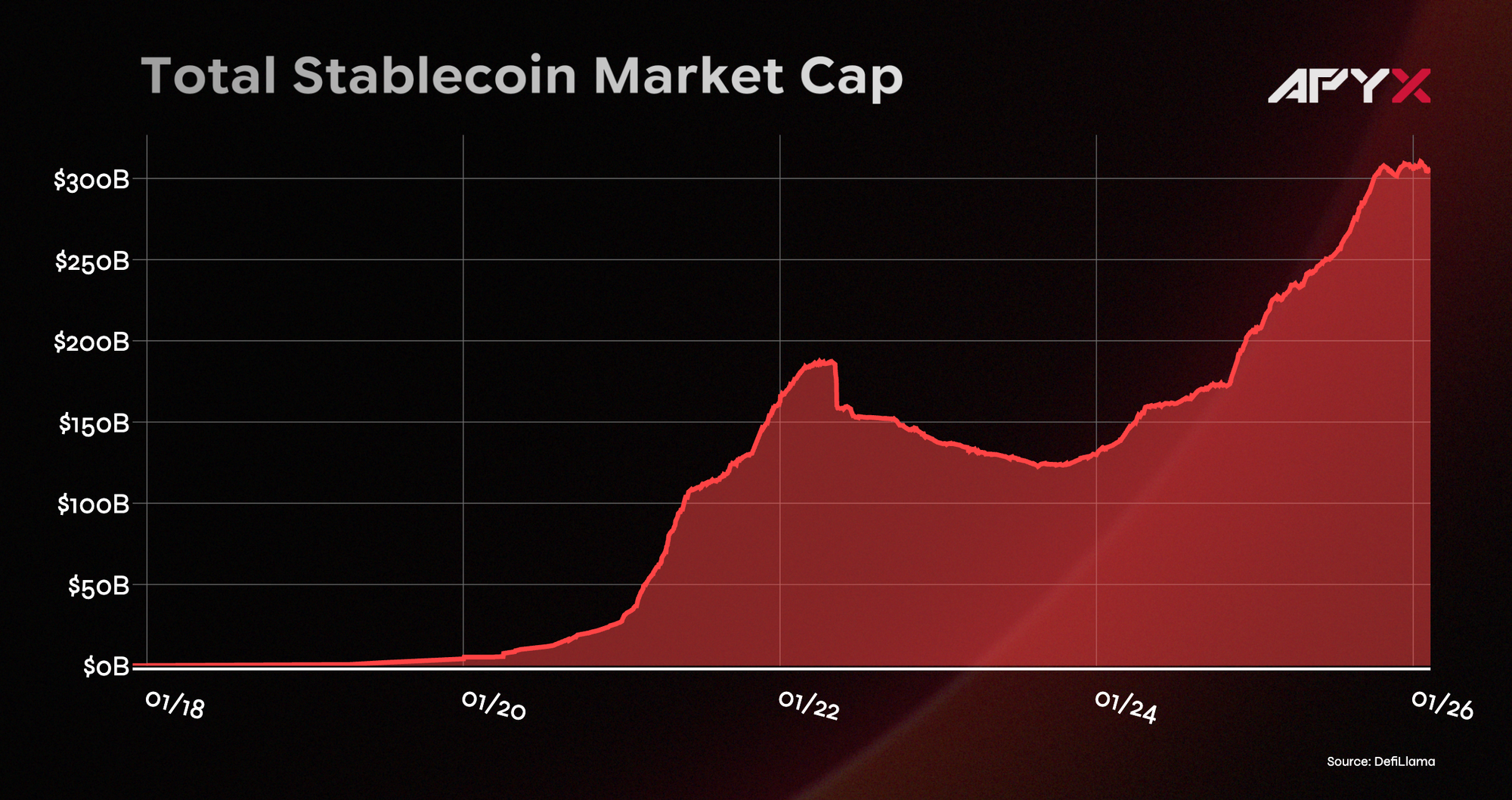

As of February 2026, the stablecoin market has ballooned to nearly $310 billion, with roughly 85% concentrated in non-yielding USDT and USDC. Stablecoins, among other things, removed volatility, enabled payments and settlement for users without reliable access to banks, and standardized collateral across onchain finance. Much of crypto's success to date can largely be attributed to the birth and rise of stablecoins.

But as the market has grown, a structural problem has become harder to ignore. Passively holding stablecoins means not only an opportunity cost, but also a loss of purchasing power. Currently, to generate yield on the vast majority of stablecoins, users must take on extra risks via a lending platform or liquidity provisioning. With more than $300 billion in capital stuck in zero/low yielding stablecoins, a disconnect grows between the capital's scale and the rails for delivering yields. This is essentially the "eroding money problem," where assets lose value relative to inflation.

The burden of a non-yielding stablecoin becomes especially apparent when accounting for inflation, which has averaged 3% annually for the past decade. Normally, market participants park capital into cash-like products, such as T-bills or money market funds, to minimize the burden of inflation. Though better than the near 0% rate offered in a traditional savings account, money market products still deliver underwhelming returns that fail to outpace inflation.

This is what we call "The Trillion Dollar Yield Crisis." Onchain dollars have become the default medium for crypto and will keep growing into the trillions, but it is still unclear how dollar savings can become the default at scale and preserve value without forcing users into increasingly risky behavior.

Delta-Neutral Synthetic Dollars Proved Demand, but Hit a Scaling Wall

To close this gap, delta-neutral synthetic dollars surged in popularity. They embed yield directly into the dollar by combining sources like staking yield and funding rates, so users can hold a yield-bearing dollar without running complicated strategies themselves.

The issue is what these models rely on to generate returns. Delta-neutral designs draw yield from market-structure opportunities such as funding, carry, and basis, plus the ongoing work required to maintain the strategy, including hedging, rebalancing, and trading. As more capital crowds into the same opportunities, spreads tighten, funding moves toward equilibrium, and market impact and operating costs rise as position sizes grow.

Over time, that creates structural pressure: as the system scales, yield tends to fall. In other words, this model successfully proves demand for yield-bearing dollars, but it is structurally disadvantaged as a foundation for a trillion-dollar baseline yield rail.

The Key

Sustainable Yield Starts With Digital Credit

The key to bridging this gap lies in DATs and the Digital Credit they produce. DATs do not stop at simply holding digital assets like Bitcoin. They place those holdings at the center of their financial strategy and expand them through capital markets funding.

For this model to work, the market must value the company above the net asset value (NAV) of its holdings, creating an mNAV premium. When that premium holds, the company can raise capital on favorable terms to buy more assets. Performance supports expectations, expectations unlock funding, and funding expands holdings, creating a growth loop. But when the premium weakens, the dynamic changes. New issuance is perceived as dilution and expansion becomes burdensome.

Enter variable rate perpetual preferred stock: Strategy's STRC (Stretch) exemplifies this approach most concretely. Strategy positions STRC as "Short Duration High Yield Credit" or "Bitcoin-backed Money Market," paying dividends monthly in cash and adjusting rates each month to keep the price trading near its $100 par value. STRC has no expiry date, so Strategy never has to repay the preferred. As of February 2026, STRC's indicated dividend rate is 11.25%. Saylor refers to STRC as "Digital Credit," indicating that DAT preferred stock competes with bonds and money market products.

Strategy announced building a $1.44B Reserve to support preferred dividends and debt interest payments starting December 1, 2025, funded by common stock ATM sales. In practical terms, this means Strategy holds enough cash on hand to keep paying dividends for at least 12 months without needing to sell any Bitcoin or issue new equity — with a long-term goal of extending that runway to 24 months or more. By managing liquidity, payment capacity, and dividend structures as a unified set, the issuer creates a Digital Credit layer.

As the DAT model grows and common stock issuance conditions tighten, the center of gravity for expansion inevitably shifts toward more credit tools.

The Solution

Turning Digital Credit Into a Native Onchain Yield Rail

Digital Credit is powerful, but in its current form it remains largely confined to traditional markets. DAT preferred equity generates recurring cash dividends that are structured, transparent, and scalable. Yet those cash flows sit offchain in brokerage accounts, rather than flowing into the onchain economy.

Apyx bridges that divide.

Rather than depending on crowded basis trades or reflexive funding markets, Apyx anchors itself to the dividend layer created by DAT preferred equity. The protocol acquires preferred shares, aggregates their recurring cash flows, and converts those offchain dividends into programmable onchain yield.

The architecture is simple but game-changing. Digital assets reside on public balance sheets. Preferred equity finances their accumulation. Dividends are paid in cash. Apyx transforms those cash flows into a native onchain savings rail.

This is not a short-term trade. It is a structural connection between public capital markets and DeFi. As preferred issuance expands, dividend streams grow. As those dividend streams grow, the depth and resilience of onchain yield strengthen. More compelling dollar savings reinforce demand for the preferred layer that supports it.

That reinforcing loop is the "Digital Credit Flywheel."

For the first time, recurring cash flows generated in public markets can directly power onchain savings. Stablecoins reaching a trillion-dollar market is inevitable. The more important question is where the yield that underpins that growth will originate, and who will capture it. Apyx answers that question.

DATs Are Here To Stay

DATs are often misunderstood. Currently, many market participants believe that they're merely ticking time bombs. If crypto falls, they will be forced to liquidate. They will accelerate the bear market. They will unravel like FTX or 3AC. That framing confuses fundamentally different structures.

DATs are not offshore lenders running opaque leverage against short-term liabilities. They are public companies with disclosed capital structures, defined debt hierarchies, and visible asset coverage — meaning the value of their Bitcoin holdings is large enough to back what they owe, and anyone can verify that on a public balance sheet. Their liabilities are structured instruments, not margin accounts. Most importantly, they are designed around accumulation, not liquidation.

The DAT model only works if digital assets are held and grown per share over time. Selling crypto is economically destructive. It compresses mNAV, weakens investor confidence, reduces credit flexibility, and can create reflexive downside. Management teams understand this. Shareholders understand this. The capital structure is built around long-term asset growth, not forced turnover.

Be that as it may, that does not mean DATs are risk-free. In an extreme and prolonged downturn, if asset coverage deteriorates — meaning the value of their Bitcoin holdings falls to the point where it no longer comfortably backs what they owe — and fixed obligations cannot be met, impairment is possible. Preferred equity sits below debt. Bankruptcy risk, while remote for well-structured issuers, is not zero. But that is a credit analysis question, not a structural inevitability.

The narrative that DATs will mechanically unwind in a bear market assumes automatic liquidation triggers that simply do not exist in most major structures. Debt service obligations matter. Asset coverage matters. Liquidity management matters. Price volatility alone cannot force sales.

More broadly, DATs represent the integration of digital assets into public capital markets. Once preferred issuance deepens and dividend streams become embedded in portfolios, these structures become part of the financial architecture. That said, it's important to note that credit markets tend to persist through cycles.

In short, digital assets are becoming permanent treasury holdings for public companies. As that trend matures, the preferred layer that finances them matures with it. That is not a speculative cycle. It is capital structure evolution. For these reasons, we remain confident that well-structured DATs can operate through bear markets and continue accumulating responsibly. As capital structures evolve, preferred equity is emerging as the natural funding layer for long-term digital asset accumulation. Apyx is designed to participate in that evolution and help deepen the liquidity that makes it possible.

What Makes Apyx Different?

Apyx is supported by the team behind DeFi Development Corp. (Nasdaq: DFDV), the first SOL DAT. As such, Apyx consists of a team of Crypto and TradFi veterans with deep experience in capital markets, digital assets, and the DAT model. Having operated at the intersection of public markets and crypto, we understand not only the opportunity in stablecoins, DATs, and Digital Credit, but also the frictions, inefficiencies, and structural weaknesses that persist. Apyx is built from that vantage point.

Unlike most stablecoins that offer little to no native return, and unlike many crypto yield products that rely on complex or black box trading strategies, Apyx delivers enhanced yield anchored to the dividend layer created by publicly traded DAT preferred equity. Yield is not derived from opaque leverage loops or reflexive market dislocations. It is tied to recurring dividend streams generated within transparent public capital structures. Users no longer need to rely on strategies they cannot fully inspect or question whether returns adequately compensate for risk.

Transparency is embedded into the structure itself. The protocol provides daily NAV reporting, real-time visibility into underlying collateral, verifiable holdings of exchange-listed securities, and regular third-party attestations. There are no hidden trading engines or undisclosed leverage layers. Users can clearly see what backs the system and how yield is generated.

That foundation has enabled Apyx to secure an elite group of launch partners. We are working with experienced infrastructure providers and DeFi venues to support reliable issuance flows, deep liquidity, and a strong user experience from day one. The result? A stablecoin designed to combine enhanced yield, public-market accountability, and institutional-grade transparency while remaining competitive at scale.

What’s Next

- Apyx is slated to launch on Ethereum in February 2026, with support on Solana to follow shortly thereafter.

- We will publish our technical documentation on GitBook, along with an FAQ that goes deeper into the mechanism design.

- Accounting attestation reports with third party auditors will be published monthly and announced via our social channels.

- At any time, you will be able to view key metrics such as total reserves and the Protocol Backing Ratio on the transparency dashboard.

- After the public launch, we will host weekly or bi-weekly Leadership AMAs.

Want to know when Apyx launches? Subscribe to our email newsletter.

For additional updates, be sure to follow us on Twitter, as well as join our Discord and Telegram to learn how you can get involved in the Apyx community on day 1.