Strategy & STRC: Everyone’s Wrong, But We’re Right.

It would appear as though even the smartest people in the industry have decided Strategy is dying.

As of the time of writing, STRC trades at roughly $84 (−16% below par) and MSTR remains within striking range of 1x mNAV after retracing nearly −60% in less than a month. Anywhere you look, you are bound to see claims of "death spiral," “Strategy is going to get liquidated,” "Ponzi," "the peg broke," "exit liquidity," and more. Crypto Twitter has held the funeral, ordered the flowers, and has moved on to which once relevant Key Opinion Leader (KOL) or underperforming investment fund called it first.

Here is the thing almost nobody in that thread understands: a lot of the bears built a genuinely good map of how this machine works. They traced the funding flows, the senior claims, the reflexivity, the procyclical issuance. And then they read their own map upside down only to mistake a mechanism for a verdict. Said differently, they correctly described the engine and then declared, with total confidence, that it must explode.

The reality is simpler: the STRC fears are mostly overblown. Unless bitcoin falls back to 2022-era levels and stays there for years, Strategy is not close to a material wind-down. In this article, we take the real risks seriously, dismantle the lazy takes, show the math that actually matters, and lay out exactly what would have to happen for us to be wrong.

First, Let’s Get This Out of the Way…

The bear case has teeth in four specific spots, and an honest analysis names them before it answers them. It should be noted, however, that none of these risks are imaginary. They are real, measurable, and deserve to be taken seriously. But the question isn't whether they exist, the question is whether they are fatal. We don't believe they are.

1. The Carry Is Real

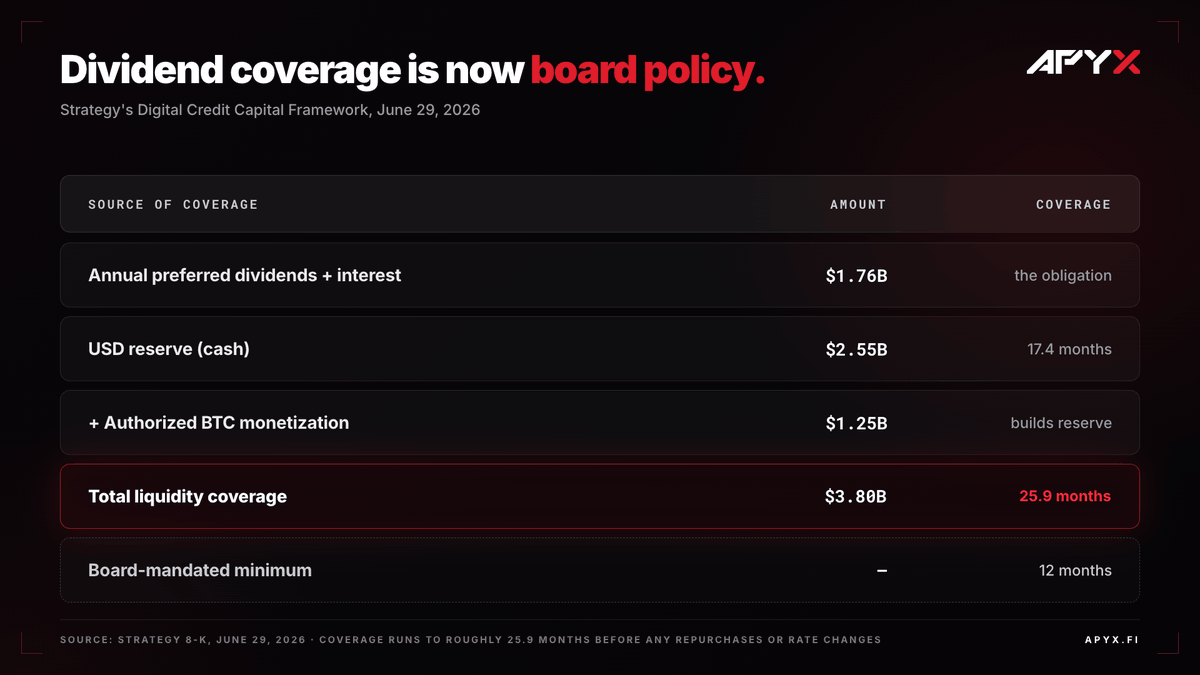

STRC is a perpetual preferred with no maturity date, no scheduled principal repayment, and an ongoing dividend obligation while the shares remain outstanding. At roughly $10.5B outstanding and a 12% coupon, that amounts to approximately $1.26B of annual STRC dividends alone. Including debt interest and other preferred obligations, Strategy estimates roughly $1.76B of annual fixed financing costs. That cash must ultimately be funded against an asset, bitcoin, that generates no cash flow of its own. During a prolonged downturn, those obligations don't disappear. They continue while reserves are consumed and financing flexibility can deteriorate. This is a real risk and shouldn't be dismissed.

2. The Issuance Channel is Procyclical

Strategy issues STRC at par. Once it trades below par, issuing additional STRC becomes unattractive. The easiest time to raise preferred capital is when markets are healthy and the hardest time is precisely when liquidity is needed most - that asymmetry is real.

3. The Flywheel is Premium-Dependent

Issuing common equity only increases bitcoin per share when MSTR trades above its underlying asset value. As that premium compresses, equity issuance becomes less attractive. Below the breakeven point, it becomes dilutive. The flywheel therefore accelerates in strong markets and slows in weak ones. Reflexivity cuts both ways.

4. The Converts Have A Clock

Strategy's convertible notes begin reaching put and maturity dates in a few years. If MSTR remains well below their conversion prices as those dates approach, some of those obligations could require cash repayment rather than equity conversion. That introduces refinancing risk and deserves careful attention.

Now, The Lazy Takes…

The problem is that the legitimate analysis became distorted as it spread. Nuanced discussions of reflexivity, funding risk, and capital structure were stripped of their qualifications and reduced to blanket predictions of collapse. That's the version that went viral and it's also the version that's wrong.

“It’s a Death Spiral. They’ll Be Forced to Liquidate.”

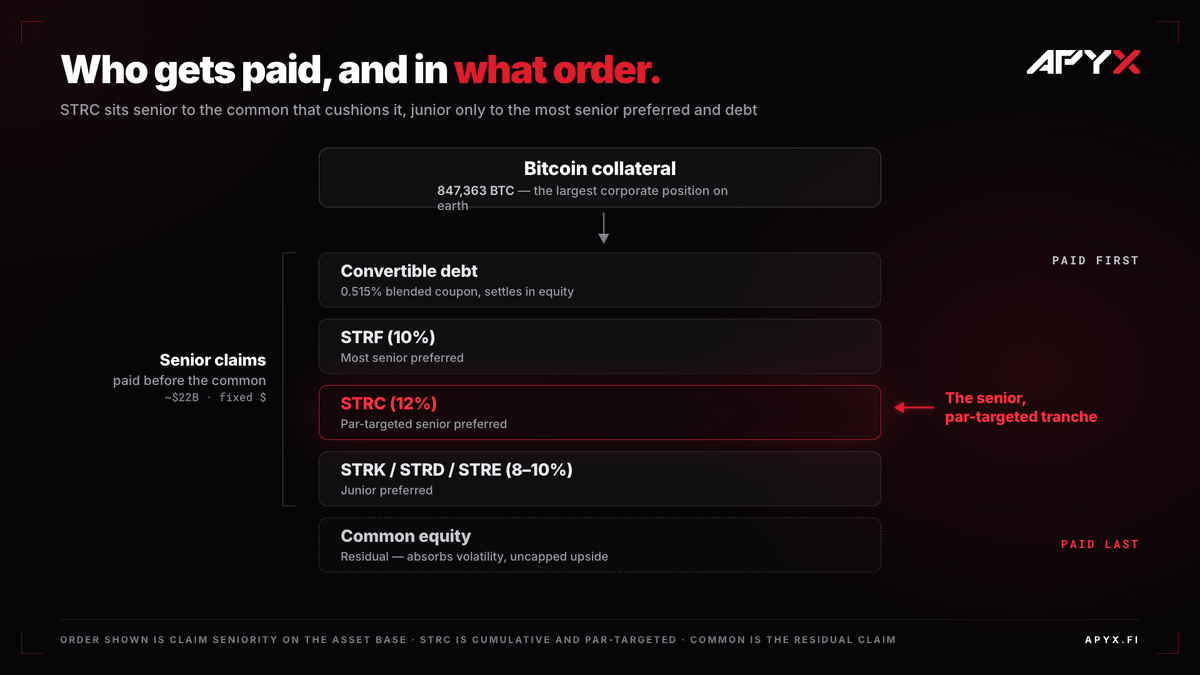

This argument imports the mechanics of a leveraged margin account into a capital structure that has none. STRC is preferred equity, not debt. There is no margin call, no collateral trigger, and no contractual mechanism forcing Strategy to liquidate bitcoin because the preferred trades below par.

A discounted STRC can make raising incremental preferred capital more difficult. It can increase funding costs. It can narrow management's options. Those are legitimate concerns. What it cannot do is trigger a forced unwind. Nobody can accelerate repayment of an instrument that has neither a maturity date nor a redemption mechanism.The entire language of "forced selling" is borrowed from instruments with contractual liquidation mechanics that STRC simply doesn't have. Calling this a "death spiral" mistakes reduced financing flexibility for forced insolvency.

“The Debt Is a Time Bomb.”

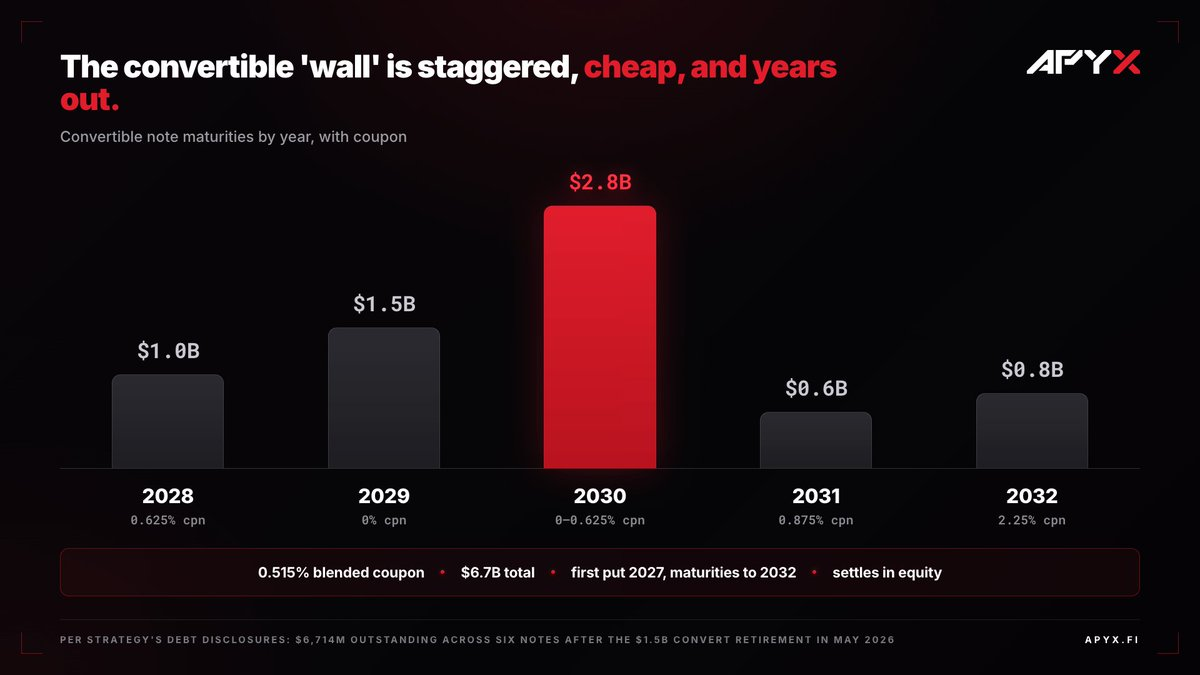

The convertibles are arguably the strongest part of Strategy's capital structure, not the weakest. Their blended coupon stands at 0.515%, annual cash interest is measured in tens of millions of dollars, and no meaningful maturity wall arrives until 2028. Management has also repeatedly stated its preference to settle these securities through equity conversion whenever possible.

Strategy has already demonstrated another path. In May, it retired approximately $1.5B of convertible notes below face value, reducing future obligations while spending less than par. That transaction wasn't an exception, it illustrated one of several tools available to the company. The real risk isn't the coupon, but the principal.

Beginning in 2027 and 2028, noteholders gain put and maturity rights. If MSTR remains below the applicable conversion prices as those dates approach, holders will choose cash repayment instead of equity conversion. That transforms an equity-linked security into a cash obligation. Serious skeptics focus on this risk, and rightly so.

What often gets overlooked is that Strategy has multiple ways to address those obligations.

- Time: The maturities are staggered from 2028 through 2032 rather than concentrated into a single refinancing wall. Any meaningful recovery in bitcoin during that period could place the notes back in the money, allowing them to settle through equity rather than cash.

- Discounted Purchases: During stressed credit markets, convertible notes themselves frequently trade below par. Strategy has already shown it can retire obligations below face value, shrinking liabilities accretively instead of repaying them dollar-for-dollar.

- Bitcoin Monetization: The June 29 authorization provides a non-dilutive funding source. Selling a relatively small portion of an 847,363 BTC treasury can satisfy obligations without issuing common equity into market weakness.

- Refinancing or Equity Settlement: the conventional corporate finance solution.

Only that final lever becomes materially more difficult in a prolonged bear market. The other three remain available regardless of market sentiment. For that reason, the convertibles resemble a manageable, scheduled liability far more than the existential "time bomb" they're often portrayed to be.

“The Peg Broke… It’s Over.”

To reiterate, STRC is a variable-rate, par-targeted perpetual preferred. The term “targeted” does not mean “pegged”; the dividend adjusts over time to pull demand back toward par. Calling its discount a 'broken peg' is not just categorically wrong, but misframes the instrument entirely. The decline from par wasn’t the market saying the instrument failed, it was saying it wanted a higher yield. Given STRC’s impact to date, Strategy has every incentive to support a return to par and the company has raised the dividend seven times since launch specifically to close gaps like this one - with the latest increase being 50bps to 12% effective July 1, 2026.

{kind=link}

Unlike other preferreds trading at a discount with no comparable mechanism pulling them back, STRC has both the structural lever and management's stated intent pointed in the same direction. That doesn't guarantee a return to par and Strategy states that in its own filings. But it does mean the discount reflects a yield negotiation in progress, not a structural failure. Where bears will find themselves in trouble is when STRC inevitably returns back to par and what was alleged to be "permanently broken sentiment” is thrown out the window entirely.

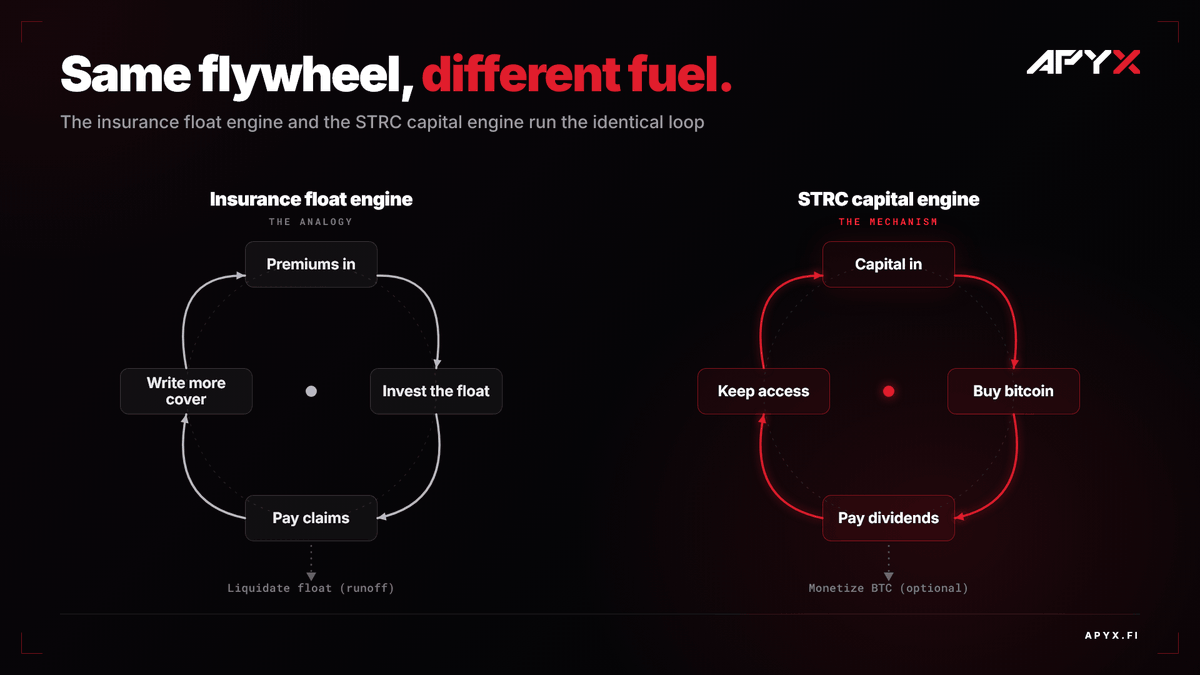

“It’s a Ponzi. New Buyers Pay Old Holders’ Dividends.”

The honest version of this is that when dividends are funded partly through fresh issuance, new capital services prior obligations, which also describes a great many dividend-paying companies running an At-The-Money (ATM) offering. There is, in fact, a respectable, centuries-old business that runs on exactly this topology: insurance.

An insurer collects premiums up front, invests the pool of capital it holds against future claims (the float), and pays those claims over time from a combination of new premiums and the returns on that invested float. New money services prior obligations, and a large pool of real assets stands behind the promise. Capital raised through issuance funds the dividend, the bitcoin stack is the invested float standing behind the obligation, and when it is the more advantageous source, a small and authorized slice of that float can be monetized to meet a payment.

{kind=link}

The defining feature of a Ponzi is the absence of assets, not the presence of new inflows. "Ponzi" means something specific: no real assets, nothing behind the payout but the next deposit. Excluding cash, STRC is over-collateralized by 847,363 BTC, the largest corporate bitcoin position on earth, tens of billions in the most liquid, most verifiable collateral that exists, senior to the common beneath it. The analogy is not flawless, since an insurer earns an underwriting spread while Strategy's spread is a directional bitcoin bet, but on the specific charge that a circular structure must be fraud, insurance is the counterexample that ends the argument. Call the structure leveraged, reflexive, premium-dependent, all fair and all true. But "Ponzi" is just a word people reach for when they want the dunk without the homework.

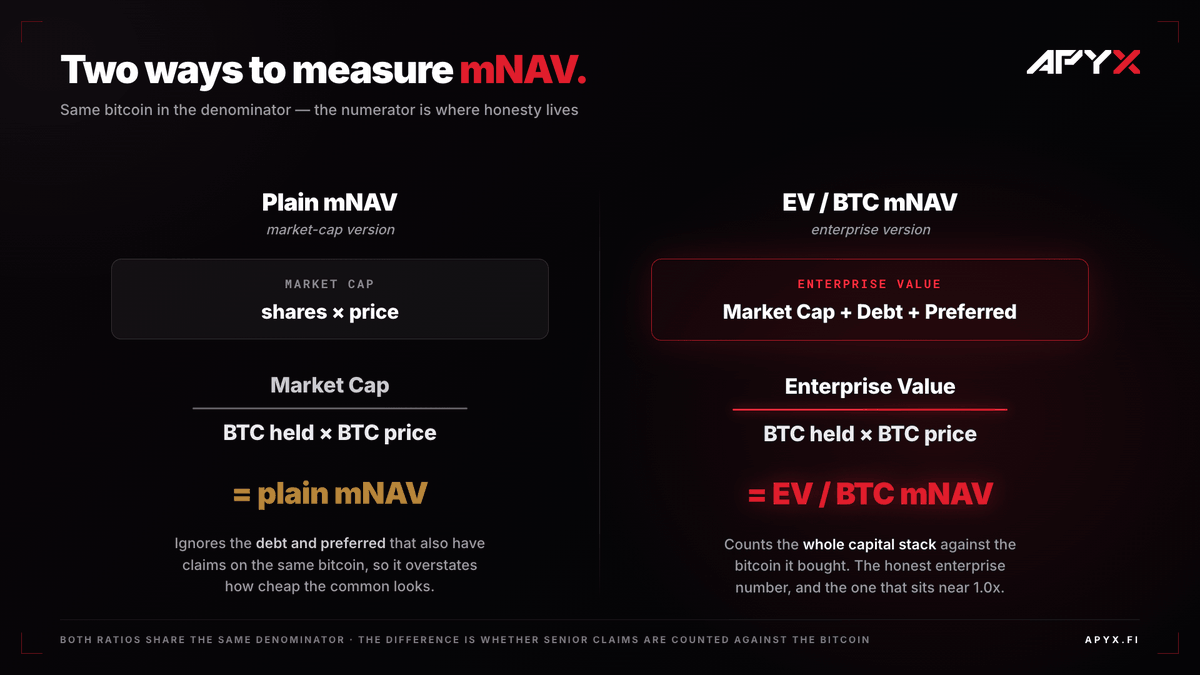

“mNAV Is Made-up and It’s Collapsing.”

Two claims here: that Strategy "moved the goalposts" by shifting from the market-cap version of mNAV to an enterprise-value version (EV/BTC), and that the metric is falling apart anyway - both miss.

The framing changed because the company did. Market cap over bitcoin worked when the structure was simple: common plus a slug of converts. Today Strategy sits on a layered preferred stack (STRC, STRF, STRD, STRK) on top of those converts, each with its own seniority and claim. Valuing the whole enterprise off market cap alone is no longer purer, it is wrong, because it ignores the majority of the claims sitting between bitcoin and the common holder.

The EV/BTC version of mNAV fixes exactly that: it counts the entire stack, debt and preferred included, against the bitcoin those instruments were issued to buy. That is honest accounting, and notably the less flattering one, since it stops the company from hiding the senior claims inside a market-cap number. You do not adopt the harder metric to spin people.

{kind=link}

As for "collapsing": it has compressed, and may stay soft a while longer. But compression is not collapse, and mNAV near 1 means the old premium is already gone, the downside largely realized rather than postponed. What remains is asymmetric; so long as bitcoin is not entering a genuine multi-year downtrend, and nothing in the macro or on-chain picture says it is, the risk from parity is skewed up.

The reason is leverage. The senior claims are fixed in dollars; the bitcoin behind them is not. When sentiment turns and bitcoin firms, the common captures a widening share of the gains and re-rates back to a premium, one that tends to persist once it returns. That premium is the single most powerful tool in the model, because it lets Strategy issue equity above the value of its bitcoin and convert the premium straight into more bitcoin per share. The flywheel the bears call broken is the one that re-engages the moment sentiment turns.

What We Believe To Be True

Having separated the real risks from the lazy ones, here is where we actually stand. These are the views we hold with conviction, and the dynamics we think the market is currently mispricing.

Sentiment Is Wrong, and Wrong for Structural Reasons

The prevailing mood around Strategy and STRC is built on inaccurate assumptions and uninformed takes rather than critiques of substance. This is a recurring pattern in crypto: when a structure is genuinely nuanced, most participants miss it, and the loudest voices have every incentive to lean into the miss. Negative narratives travel further than measured ones, because people are wired to weight threats more heavily than reassurance. That bias is a gift to anyone building an audience, which means there is a standing incentive, beyond simple laziness, to manufacture fear around the most visible target in the market. The serious mechanical critiques we credited earlier are the exception. The bulk of the noise is not analysis, and we think it will be shown to be wrong.

The Bond Market Is Not Pricing Distress

The credit market, which tends to be a soberer judge of solvency than equity traders or social media, is not pricing distress. Strategy's roughly $6.7 billion of convertible notes carry a blended coupon of just 0.515%, among the lowest financing costs in corporate America, and the entire complex trades in a tight band between about $86 and $102, with the nearest maturity, the 2028 note, bid above par at $102. That is the tell. The deepest discounts belong to the zero-coupon tranches with the highest conversion prices, while the small discounts on the coupon-bearing notes simply reflect the stock sitting below their strikes, ordinary convertible mechanics, not fear. Distressed credit trades at fifty or sixty cents on the dollar; nothing here is remotely close. When the people actually lending Strategy money price its paper near and above par, the people shorting the narrative on a chart deserve scrutiny.

The Dividend Obligation Is Small Against the Asset Base, and the Rate Is a Lever, Not Just a Cost

Measured against the bitcoin behind it, the STRC dividend is a low-single-digit percentage of the asset base per year. Even setting cash reserves aside entirely, the stack represents decades of theoretical coverage. The rate itself is also a tool: an incremental 50 basis points of yield costs roughly $50 million a year, a rounding error against the balance sheet, and Strategy can walk the rate up to clear demand whenever it chooses. That does two things at once. It refuels appetite for the instrument, and it puts to rest the recurring fear that the company must flood the market to fund itself.

{kind=link}

The Recent Weakness Was Opportunistic, Not Fundamental

The sell-off in STRC and MSTR was not, in our read, driven by any real break in the model. The narrative hook was that Strategy's "never sell bitcoin" promise had broken after it sold 32 BTC. That framing does not survive contact with the record, as Strategy sold bitcoin once before, in December 2022, for tax-loss harvesting, and repurchased shortly after. The "never sell" line was always more slogan than a covenant. What we think actually happened is more ordinary: bitcoin had run from the low-$60Ks to the low-$80Ks in a matter of months and was due a technical pullback, and that pullback handed market participants an opening to press both assets and dent a long-standing bullish narrative. Pressure on a price is not a crack in a structure, but sometimes a reflection of momentarily unsustainable bearish intent.

If Strategy Sells Bitcoin, It Will Not Break Anything

Two assumptions sit behind the death-spiral fear: that the market could not absorb Strategy's selling, and that any sale would be value-destructive - both of which are wrong. Bitcoin trades tens of billions of dollars a day and nearly $700B a month, so a monetization capped at $1.25B and spread across time and conditions is immaterial to that liquidity. And far from breaking the model, disciplined monetization keeps the flywheel turning, funding obligations and buybacks without dilution while keeping STRC holders whole. The war chest is large enough, and bitcoin's underlying liquidity deep enough, that there is no realistic path from "Strategy sells some bitcoin" to "Strategy fails."

Bitcoin Is Very Near a Cyclical Bottom

We will not pretend to call the exact day, but the weight of evidence points to a low that is in or close. Sentiment has reached the kind of extreme that has marked prior bottoms rather than tops. The market just tried and failed to bury STRC and MSTR with collapse calls. And bitcoin is trading around its long-term moving averages near $62K, within reach of the deeper support near $54K that has historically marked the floor when tested. None of this guarantees the low is set, and we state plainly in the closing section what would change our mind, but buying an asset that is hated, underwater for most holders, and pressed against support that has held every prior cycle is not catching a falling knife. Historically, it is the setup.

You Should Not Bet Against Saylor

For more than six years, Strategy and Michael Saylor have championed bitcoin and built the apparatus to acquire it at scale. In that time they took a mature, roughly $500 million-a-year enterprise software business and used the capital markets to turn it into the largest corporate holder of bitcoin in the world, with a position that now sits near 4% of all the bitcoin that will ever exist. That did not happen by accident, and it did not happen in calm conditions.

This team has navigated some of the most violent market events in recent memory and has consistently done exactly what it did again on June 29: read the market, listen to it, and refine the approach. The track record is one of adaptation, not stubbornness. People will keep criticizing them, because the most visible target always draws fire, but the criticism has been constant for years while the position only compounded. Betting against a team that has repeatedly proven it can stay nimble and think in years rather than weeks, across nearly every scenario the market has thrown at it, has been a losing trade for a long time.

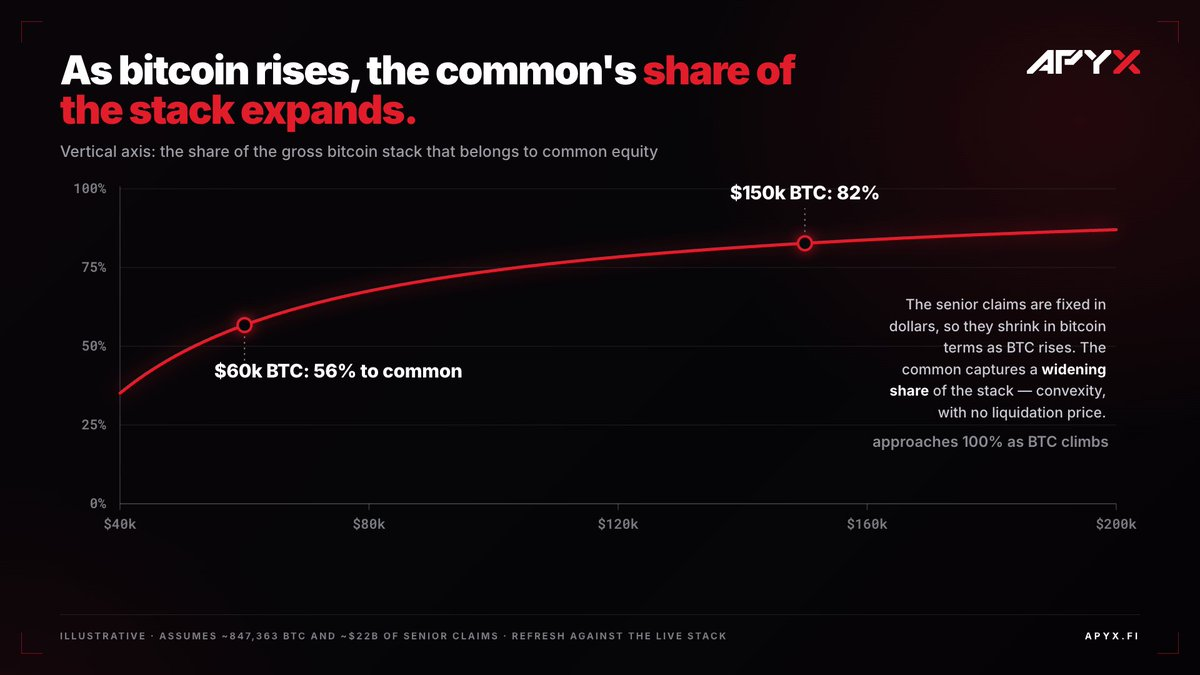

CEBE Is the Lens That Matters, It Does Two Things At Once

It dismantles the bearish narrative wholesale, and it values MSTR correctly for the company that exists today rather than the simpler one that existed before the preferred stack. That lens is common equity bitcoin exposure, or CEBE.

The usual numbers no longer fit the company. Market-cap mNAV worked when Strategy was common plus a slug of converts, but with STRC and the rest of the preferred suite layered in, the majority of the claims now sit between the bitcoin and the common shareholder, and a market-cap metric cannot see them.

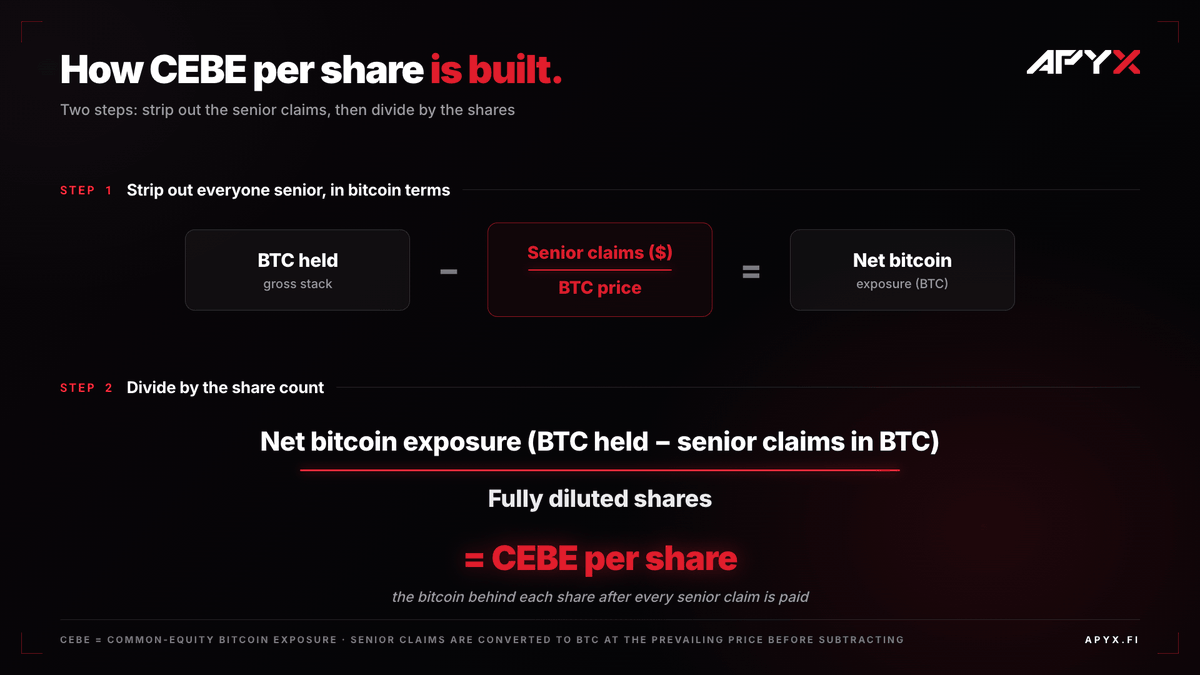

Even enterprise-value mNAV, the honest enterprise-level number, folds those senior claims into one figure: it tells you what the whole business is worth against its bitcoin, not what a common holder owns once everyone senior is paid. CEBE is the lens that does. The calculation is simple: take the gross bitcoin stack, subtract the senior claims (debt plus preferred) in bitcoin terms, and divide by the share count. What remains is the exposure that belongs to the common holder after every senior claim is satisfied. The objection that this is "made-up" is empty. The name is new; the math is net asset value per share, the same calculation used on any leveraged closed-end fund. It answers the only question a common holder should care about: after the senior claims, what is mine?

What CEBE reveals is the feature the bear case overlooks, which is convexity. The senior claims are fixed in dollars; the bitcoin behind them is not. When bitcoin rises, those fixed claims shrink in bitcoin terms and the common's share of the gross stack expands quickly, from just over half near a cycle low to the large majority of it as bitcoin climbs. This is not margin leverage. There is no liquidation price, no call, no forced unwind. It behaves like a perpetual call option on bitcoin struck above the liability stack, which is precisely why MSTR has historically moved at roughly 1.5x bitcoin's beta.

From there CEBE disposes of the bear claims rather than arguing with them. The "death spiral" requires a liquidation mechanism a call-option structure does not contain and the "dilution" complaint does not survive contact with the right metric, because dilution is measured by CEBE per share, not share count. That is the crux of the charge making the rounds now: that a recent equity sale put only about half its proceeds into bitcoin and shortchanged common holders, but it did not.

{kind=link}

The test is not what fraction bought coins, it is whether the raise lifted CEBE per share. When the stock trades above its CEBE backing, every share is sold for more than the claim it creates, so the exposure behind each existing share rises, whether the cash buys coins or sits on the balance sheet. And parked cash is not dead weight: it sits against the senior claims and de-risks them, which lifts the residual that belongs to the common. A 50-50 split, for example, is not a leak, it is accretive issuance paired with a de-risking of everything senior to you. The only world where issuance dilutes is a sale below CEBE backing, which is exactly the discipline the June 29 framework committed to avoid: near 1x mNAV, the company guides toward buying common back, not selling it.

The loudest charge, that the common holder is being sacrificed, has the logic backwards. The common does absorb the residual risk, but that volatility is the price of uncapped upside, and every claim it sits beneath is a claim that gets paid first. STRC sits above that residual, cushioned by the common equity below it and the bitcoin stack above it. The very thing that makes the common volatile is what makes the senior preferred safe. If you accept the bears' own analysis of where the risk lives, the conclusion is not to avoid the structure, it is to sit senior in it - that is STRC.

So CEBE is not just another metric. It is the correct one for a company rebuilt around instruments like STRC, and in pricing that structure honestly it answers most of the bear case in a single stroke. It also reframes how Strategy has actually performed. Judged by share price against a falling bitcoin, the past year reads as failure. Judged by CEBE, the metric that measures what a common holder truly owns, the multi-year record is one of accretion: more bitcoin standing behind each share over time, accomplished while building an entire senior capital structure on top of it.

{kind=link}

That is the execution that matters, and it is invisible to anyone still staring at the stock chart. The honest caveat is that easy accretion pauses near parity, where issuance and buybacks roughly offset, which is the regime we are in now. But that is not a failure of the model, it is the moment the June 29 discipline takes over: issue above CEBE backing, repurchase below it, defend STRC, and let the convexity do the work when bitcoin turns. By the only scorecard that prices the real structure, Strategy has delivered, and has now hard-coded the policy to keep delivering.

{kind=link}

This Was Always a Bet on Bitcoin. It Still Is.

Every bear thread eventually collapses to one load-bearing assumption: that bitcoin stays down long enough for the carry to do its damage. Strategy’s June 29 framework just pushed that “long enough” out to years and gave the company tools to extend it further. So pull the assumption and look at it directly, because the macro is the strongest leg here and the one the STRC-doomers spend the least time on.

Bitcoin is the only monetary asset in existence with no supply response to price. When gold runs, miners dig faster and flood the market. When equities run, companies print shares. When anything else gets expensive, more of it appears to cap the move. Bitcoin can’t do this, the price can scream to any level and not one extra coin enters the schedule. That single property, absolute enforced scarcity, is why it has recovered from drawdowns north of 80% every single time and gone on to new highs, and why the people calling for zero have been wrong at every prior bottom that looked exactly this grim.

And this drawdown is structurally milder than the ones before it. The 2022 cascade of Celsius, Three Arrows Capital (3AC), FTX, and forced liquidations detonating in sequence has no equivalent this cycle. There is no insolvent lender dumping coins into a bidless market. Long-term holders and ETFs have refused to capitulate. Meanwhile, the standard cycle-bottom signals, including a supermajority of supply underwater and price pressing against the multi-year moving average that marked every prior bottom, are flashing the same readings they did at lows investors now wish they had bought.

If bitcoin does what it has done every prior cycle, the fixed senior claims shrink in bitcoin terms, the convexity in the common re-rates, the premium that “collapsed” rebuilds, the STRC discount closes as the yield and the buyback do their work, and the structure the bears called a death trap turns out to have been a coiled spring. That isn’t hope. It’s the mechanical consequence of the one variable everything here depends on.

What Would Prove Us Wrong

We expect Bitcoin to carve out its cycle low and recover in the months ahead. We expect STRC to move back toward its $99 to $100 objective as the higher coupon, reserve policy, and buyback program take effect. And we expect MSTR to re-rate as mNAV moves back above 1. We view today's discounts as signs of market stress, not permanent impairment.We will be wrong if Bitcoin breaks down and remains there long enough to outlast the multi-year coverage the framework now provides, overwhelming both the reserve and the replenishment tools.

We will be wrong if management fails to execute the policies it has already authorized, whether by leaving the buyback idle or failing to honor the reserve framework when it is needed most. And we would view a deferred or missed STRC dividend as a genuine distress signal, not a buying opportunity, because that would indicate the cash flow supporting the structure had failed despite every tool designed to prevent it.

Notice what has changed. The bears' strongest prescription, build reserves, slow accumulation when appropriate, support the preferred, and be willing to monetize a small portion of the Bitcoin treasury, is now company policy. The debate is no longer whether the structure can work. The real question is whether management will execute the plan it has already put in place. That is a far better debate to be having.

Where We Stand

The final observation.

Strategy didn't describe June 29 as a preferred-stock update or even a balance-sheet update. It introduced a Digital Credit Capital Framework, which matters because it signals something larger than one company's financing strategy. It recognizes BTC-backed, yield-bearing senior instruments as an emerging asset class rather than a one-off capital markets experiment.

As builders in digital credit, we've viewed STRC exactly this way from the beginning. Our job isn't to react to headlines, it's to understand these instruments at the capital-structure level, stress-test them under adverse scenarios, and determine whether the market is pricing risk correctly.

After working through that exercise, our conclusion is straightforward: we remain confident in both STRC and MSTR, not because the risks don't exist, but because we believe the market has dramatically overstated them. When you separate liquidity from solvency, mechanics from narratives, and structure from sentiment, the math, the macro, and the company's own capital policy all point in the same direction.