Apyx 2.0: Redemption Value, Total Collateralization, & Evolution of the Dividend-Backed Dollar

Two weeks ago, Apyx went through the most significant stress test since launching in February 2026 and scaling to as much as $500M in circulating supply. STRC posted its largest decline from par on record, apxUSD traded as low as $0.90 on secondary markets, and the protocol processed a wave of redemptions while remaining solvent throughout. What followed was a detailed post-mortem covering what happened, what went wrong, and what went right. This post is about what comes next.

The stress test did more than expose operational gaps; it revealed that our capitalization framework needed to be more clearly defined and codified, particularly around how redemptions interact with the overcollateralization buffer during stress. What follows is not a change in the protocol's core thesis, but a clearer articulation of the rules that govern it and the framework we intend to operate under.

What apxUSD Is, Stated Plainly

It’s first worth restating what apxUSD actually is, because expectations matter and so does having users' confidence in Apyx.

apxUSD is a dividend-backed dollar backed by a reserve of income-generating preferred equity from Digital Asset Treasury (DAT) companies, as well as treasuries and cash equivalents. Those preferred shares pay real, publicly reported dividends, and that income is what powers apyUSD's yield. The reserve is transparent, attested monthly by Wolf & Co., a PCAOB-registered accounting firm, and verifiable in real time through cryptographic Proof-of-Reserves on our Accountable page.

apxUSD is not a bank deposit; the underlying collateral is predominantly STRC, Strategy's preferred equity. As of today, STRC has now traded more than 5% below par four times since being issued in July 2025, and each prior episode has resolved as the dividend mechanism pulled the price back toward $100.

The entire design of Apyx is to deliver a product with higher yield and lower volatility than the underlying basket itself: higher yield through the two token model, lower volatility through the cash portion of the reserve. A dollar backed by dividend-paying equity behaves differently than a dollar backed by overnight bank deposits, and it should be understood, priced, and used accordingly. That is not a weakness of the design. It is the design, and it is what makes double-digit sustainable yield possible in the first place.

What the Drawdown Made Clear

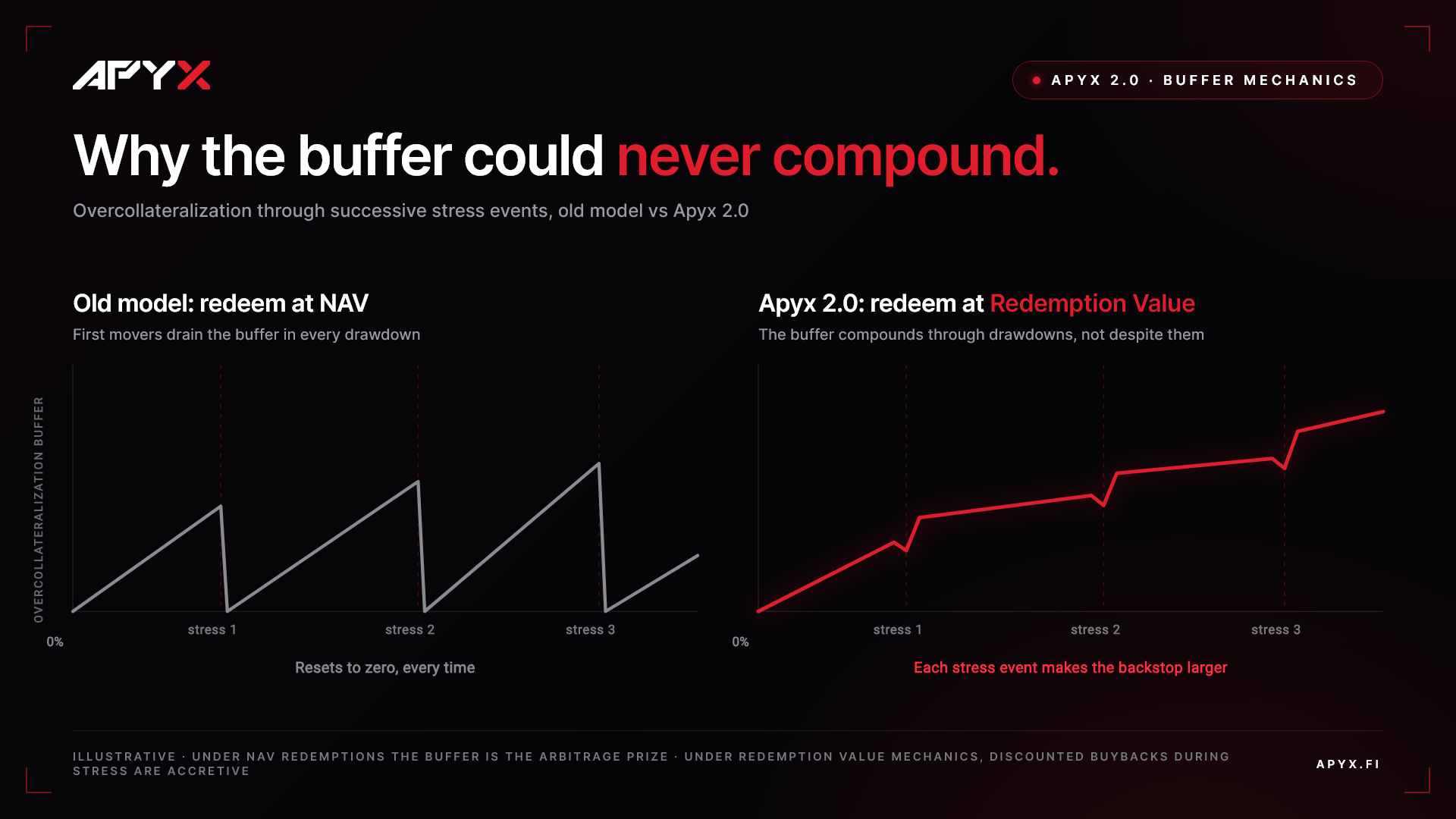

Apyx's messaging at launch was focused on a conventional overcollateralization model: hold more collateral than circulating supply, let the buffer absorb drawdowns, and grow the buffer over time. The intent was anti-fragility and the buffer was supposed to compound through stress events, not in spite of them. In the drawdown, users demanded that the overcollateralization buffer be consumed to facilitate redemptions at or above NAV.

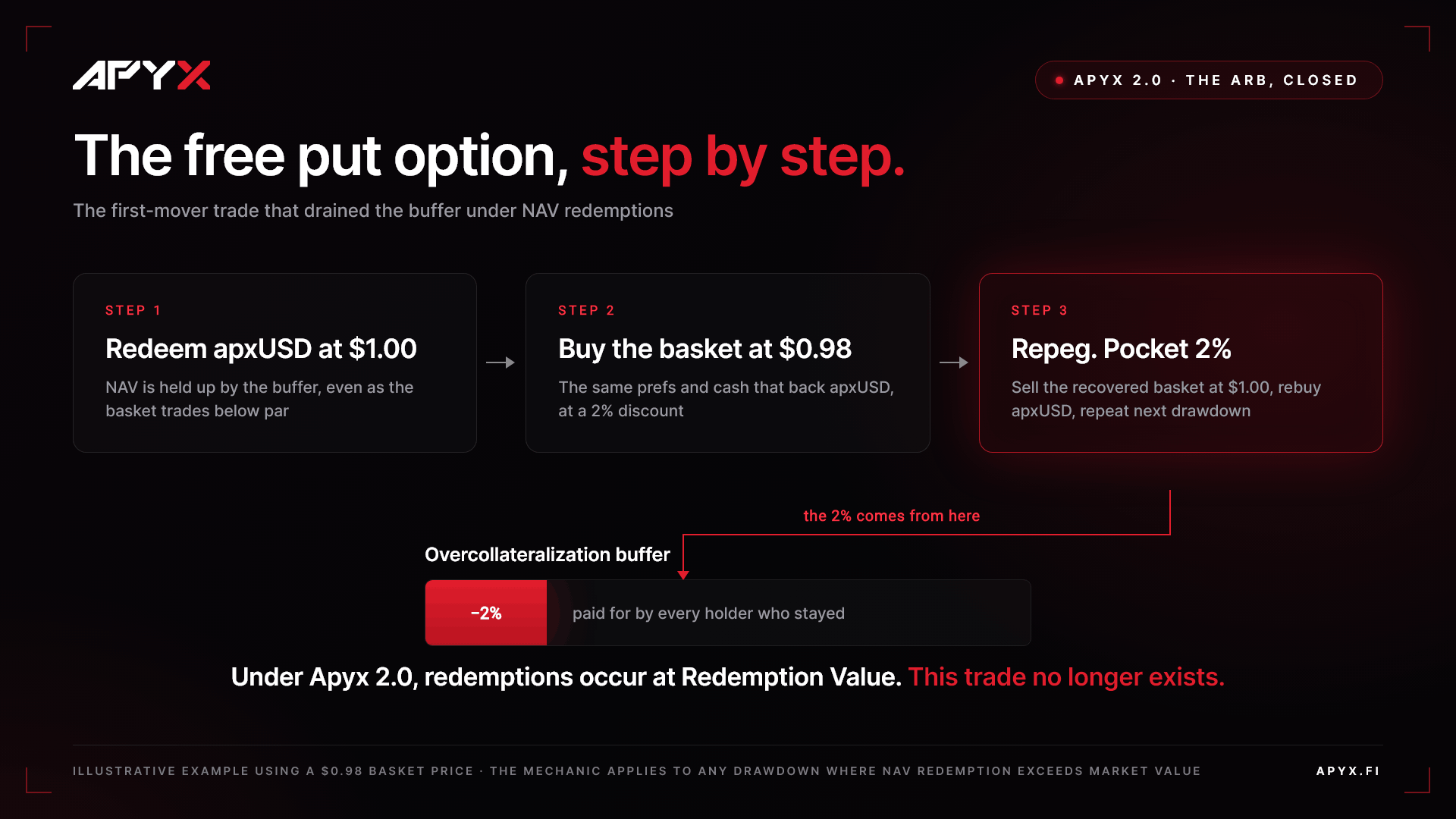

The stress test made clear why this distinction needed to be published and codified from the start. Redeeming apxUSD at a NAV that includes the overcollateralization buffer hands out a free put option during every drawdown.

Here is the dynamic, with concrete numbers. Suppose the underlying basket of prefs and cash trades down to $0.98 while the buffer holds the quoted NAV at $1. A rational first mover redeems apxUSD at $1 and buys the underlying basket at $0.98. When the basket repegs to $1, they sell it, rebuy apxUSD, and pocket 2%. That 2% did not come from nowhere. It came directly out of the overcollateralization buffer, which means it came from every holder who stayed.

Run that cycle through every drawdown and the buffer drains to zero each time, then starts over. The protocol can never compound its way to a meaningful buffer because the buffer itself is the prize. Worse, the dynamic is predatory by construction: it rewards the fastest exits at the direct expense of the most loyal holders, and it hands adversarial market participants a standing incentive to manufacture stress. A mechanism that pays first movers to drain the backstop is a mechanism that will eventually doom any protocol built on it.

During the latest drawdown, our redemption pricing did exactly what it was designed to do: protect the buffer by quoting below NAV during stress. The mechanism worked, the buffer survived the largest STRC decline in history. But we hadn't communicated that design clearly enough. Users saw one number on the transparency dashboard, saw a different number on their redemption quote, and understandably expected to redeem at NAV. The gap wasn't in the logic, it was in what we'd published about how the system behaves under pressure. We learned from that. Both from the communication shortfall and from watching how the depeg played out in practice, we've built a better framework for Apyx 2.0: one that codifies the rules, makes pricing behavior predictable in advance, and gives users a materially improved experience during stress, not just the same mechanism with better docs.

The Fix: Redemption Value and Total Collateral Value

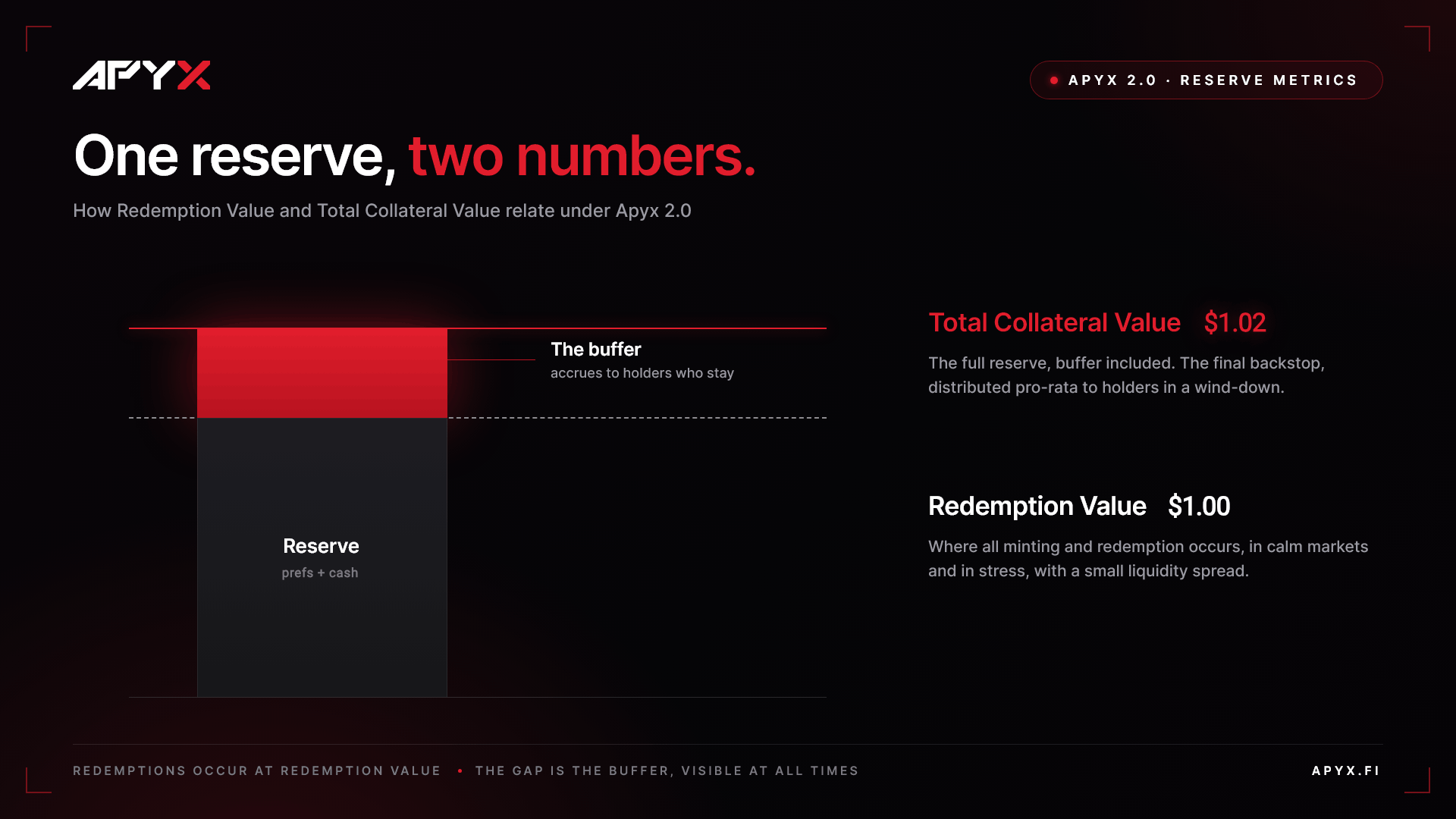

Going forward, the protocol will publish two distinct metrics on the transparency dashboard, and the relationship between them will be explicit.

Redemption Value is the price at which all minting and redemption occurs, with a small spread for liquidity and slippage purposes. This is the number that governs every interaction with the protocol's primary market, in calm conditions and in stress, for every participant. No more ambiguity about what a redemption quote will be or why.

Importantly, Apyx 2.0 will also introduce an RFQ (Request for Quote) redemption system designed to improve the user experience during periods of stress. Rather than relying solely on automated redemption pricing, users will be able to submit redemption requests through a structured RFQ process, allowing approved counterparties to provide competitive execution against the underlying reserve.

Total Collateral Value replaces NAV on the dashboard. It is the full value of the reserve, including the overcollateralization buffer. Total Collateral Value may read $1.02 while Redemption Value reads $1. The gap between the two is the buffer, visible to everyone at all times.

Because redemptions occur at Redemption Value rather than against the full collateral, the first-mover drain that NAV-based redemptions would have created is permanently off the table. There is no longer a free option to exercise against the buffer. The 2% trade described above simply does not exist under the new framework, which means the buffer can finally do what it was always designed to do: grow steadily, through drawdowns rather than despite them, compounding from retained yield, discounted buybacks, and the protocol's other activities.

So What Is the Buffer For?

The natural question follows: if holders cannot redeem at Total Collateral Value, what is the point of the overcollateralization buffer?

First, the buffer actively reduces risk for apxUSD holders without sacrificing yield. The overcollateralization buffer is 100% allocated to preferred equity, with all of the yield it generates flowing to the rest of the portfolio. As the buffer grows, the remainder of the collateral can shift toward cash while maintaining the same yield output. Picture an extreme scenario where the protocol reaches 100% overcollateralization: the buffer is fully deployed into prefs, the remainder of the collateral sits in cash, and apyUSD pays yield as if the entire basket were in prefs while taking none of the pref volatility risk. In practice, every dollar added to the buffer strengthens apxUSD's stability while making apyUSD's yield more resilient over time. Lower risk without sacrificing yield, and without creating the free-put-option situation described above.

Second, the buffer is the final backstop. In a catastrophic scenario, a devastating hack, a wind-down, or any event that ends the future viability of the protocol, Total Collateral Value becomes the redemption value, and the entire reserve, buffer included, is distributed pro-rata to everyone still holding. In the moment when the backstop matters most, it belongs entirely to the holders who are there. The governance token holders can also vote to deploy a portion of the overcollateralization buffer in "intermediate risk scenarios" to support Redemption Value.

Under NAV redemptions, the buffer rewarded whoever left first. But now, the buffer accrues to whoever stays. Every dollar of overcollateralization the protocol builds is a dollar of downside protection that loyal holders carry with them, growing over time instead of resetting to zero after every stress event. That is what anti-fragility actually looks like in practice: a protocol that emerges from each drawdown with a larger backstop, not a drained one, and a holder base whose interests are aligned with the protocol's resilience rather than racing each other for the exit.

It is worth noting that the June drawdown proved the concept in miniature. The buffer was preserved and modestly grown through the largest STRC decline on record, precisely because redemptions were not processed at full collateral value. The new framework takes what worked under pressure and makes it the published, permanent rule.

What This Changes for Holders

We want to be straightforward about what this means in practice, because setting expectations clearly is the entire point of this redesign.

Redemption Value will track the underlying basket of prefs and cash. During periods of preferred stock volatility, it will move with the collateral, dampened by the cash portion of the reserve. In practice, apxUSD should trade between Redemption Value and Total Collateral Value. Redemption Value acts as a hard floor where arbitrageurs step in, while the overcollateralized reserve supports pricing above it. New apxUSD issuance will always be priced at $1, giving the secondary market a consistent anchor. The goal is a system where the market bids apxUSD well above Redemption Value because the backing is transparent, the collateral is real, and the buffer is visible. Not one where users wait at the floor for a market maker to close the gap.

What holders gain in exchange is substantial. Clear, published redemption mechanics that apply identically in calm and in crisis, so the rules are never unclear again. A visible, growing buffer whose value accrues to those who stay rather than those who run and a protocol that no longer carries a structural incentive for adversaries to manufacture stress, because the prize that made those attacks profitable has been removed from the table.

In addition, the forthcoming RFQ redemption system will provide holders with a more flexible redemption experience by connecting redemption requests with market participants willing to transact against the reserve.

The Thesis Remains Unchanged

Digital credit represents a new paradigm shift for financial markets. Bitcoin and the major digital assets are giving rise to an entirely new class of credit instruments, and STRC growing to over $10B in under a year is the opening act, not the finale. We believe dividend-backed dollars, fully transparent, powered by real cash flows from publicly listed instruments, and accessible to anyone onchain, will take a meaningful share of the $400B behind the stablecoin and DeFi market. Most of the world remains yield-impoverished and the instruments that fix that are being built right now. Apyx is here to bring them onchain.

A protocol with that ambition needs capitalization architecture built for adversarial markets, not fair-weather ones. The June stress test compressed years of lessons into two weeks and forced us to formalize and publish the framework that makes the protocol structurally stronger than it could have been without it. The protocols that define this category will be the ones that took their stress test early, learned in public, and rebuilt better.

The next chapter of Apyx starts now.

In service of digital credit,

Apyx Foundation