STRC Myth Busting: Separating Risks From Lazy Critiques

There may not be a more misunderstood instrument in the entire investment world right now than Strategy’s STRC preferred equity.

Depending on who you ask, it is either a brilliantly engineered digital credit product designed for long-duration resilience, or a reflexive confidence scheme destined to implode the moment capital markets stop cooperating. Neither framing really captures what is going on.

A lot of the discourse around STRC suffers from the same problem: critics often identify a unique dynamic to STRC, then overextend it into a catastrophic conclusion that does not actually follow from the mechanics. Bulls, meanwhile, frequently respond by pretending the underlying concern is entirely fake, which usually weakens their credibility more than it helps. The reality is more nuanced than either side wants to admit.

STRC is absolutely reflexive, it depends on continued confidence and capital access, and it absolutely carries meaningful bitcoin-linked tail risk. But many of the loudest criticisms still misunderstand how the structure actually works, what risks are normal versus existential, and where the real pressure points truly are. In this post, we separate the legitimate risks from the lazy critiques. After reading, expect to better understand what Strategy is actually building and why STRC represents a paradigm shift in capital markets.

Myth #1: “Selling bitcoin to pay the dividend means the structure is failing.”

This critique sounds intuitive on the surface because people instinctively associate selling treasury assets with distress. But in practice, that is not how balance sheet management works.

Dividends are paid in dollars on fixed schedules. Capital raises happen opportunistically and arrive unevenly. In a structure like this, there will naturally be periods where selling a small amount of bitcoin is simply the cheapest or most efficient source of liquidity available at that moment.

If bitcoin has appreciated substantially, trimming a relatively small amount of exposure to satisfy the coupon while preserving issuance flexibility for more attractive opportunities is a rational capital allocation decision, not an emergency liquidation.

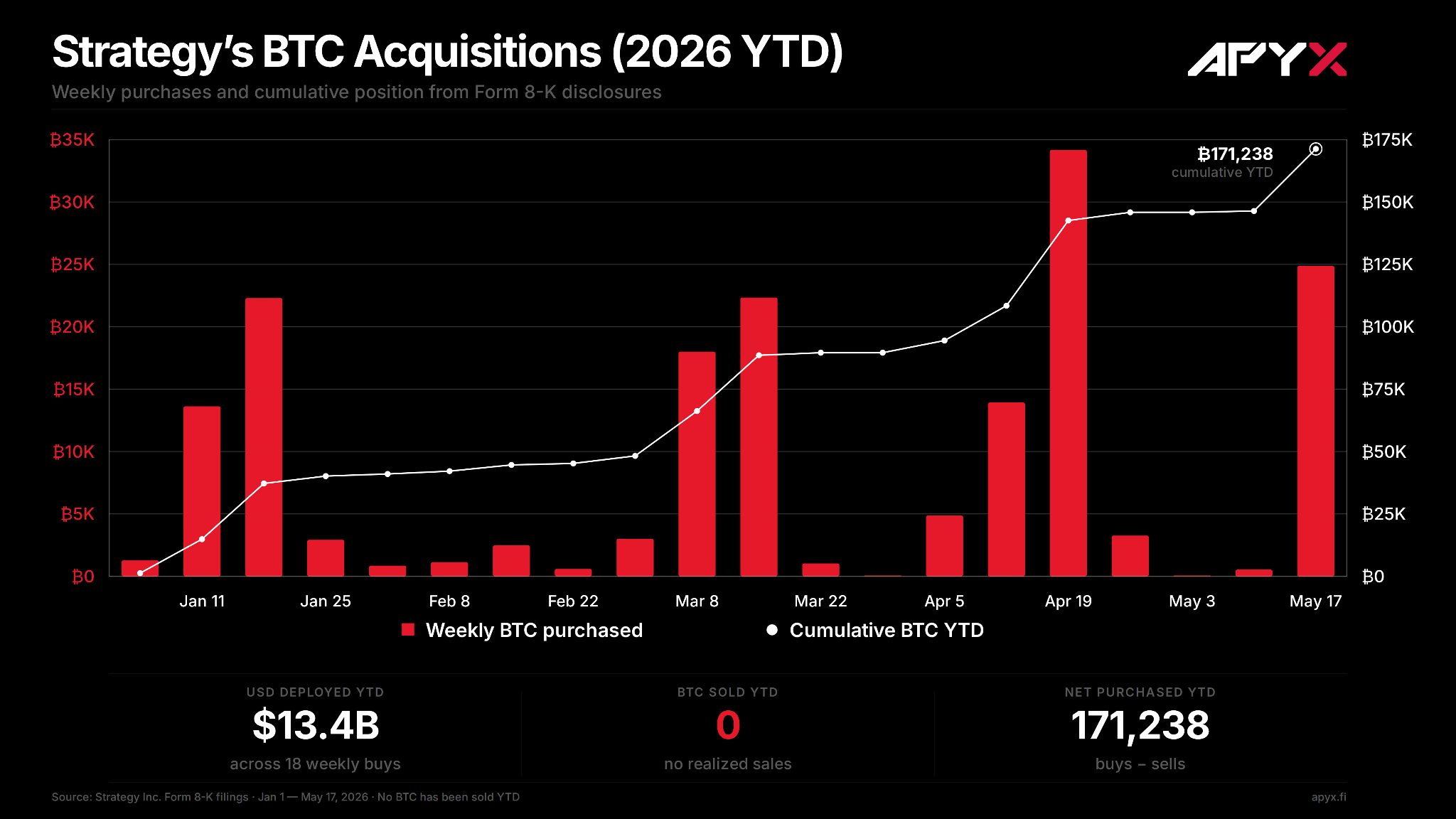

The scale matters too. Using roughly ~$950M of annual STRC dividends as a working estimate, that translates to about ~$79M per month. At $77.4K BTC, that would require roughly ~1,020 BTC per month if funded entirely through bitcoin sales. These figures pale in comparison to Strategy’s year-to-date accumulation of more than 171,000 bitcoin, let alone their treasury of 843,738 BTC. The current monthly dividend sits around 0.12% of Strategy’s bitcoin stack per month - a figure that will only dwindle as bitcoin appreciates in value. That is not nothing, but it is also nowhere close to the forced-liquidation framing critics often imply.

The May 2026 repurchase of roughly $1.5B of 2029 convertible notes for approximately ~$1.38B in cash is also a good example of the broader posture here. That was not a company desperately trying to survive. It was opportunistic liability management from a position of strength, retiring senior claims at a discount and improving the capital stack.

Where critics are directionally right is in understanding that this same mechanism can become dangerous under sufficiently stressed conditions.

If bitcoin experiences a major cyclical drawdown while issuance windows simultaneously close and reserves begin shrinking, then bitcoin sales can transition from ordinary treasury management into a self-reinforcing stress amplifier. The exact same action can have completely different implications depending on the environment. But that is also why Strategy created STRC with multiple buffers:

- Large reserves,

- Staggered maturities,

- Low coupon debt,

- And a discretionary dividend structure.

A normal crypto-cycle drawdown is fundamentally a timing problem the system was built to absorb. The structure only truly breaks under a much harsher scenario where bitcoin itself suffers a prolonged structural failure with no eventual recovery. And at that point, no bitcoin-linked preferred structure survives anyway. That is not a hidden flaw in STRC, it is the explicit nature of the bet that every purchaser understands.

Myth #2: “Preferred means you’re first in line.”

Yes, STRC holders rank behind Strategy’s convertible debt stack. But framing that as some uniquely dangerous hidden flaw misunderstands how preferred stock works universally, as preferred equity is junior to debt by definition. The relevant question is not whether STRC is subordinate; the relevant question is what it is subordinate to.

And here, the senior stack is actually relatively benign. After the latest 2029 convert repurchase, Strategy’s senior convertible layer is approximately ~$6.7B. Against a bitcoin treasury worth roughly ~$65.3B at $77.4K BTC, the bitcoin asset base covers the senior convertible layer by nearly 10x before even considering the software business, future accretion, or other capital actions.

The converts themselves are:

- Low coupon,

- Long duration,

- Staggered maturities,

- And actively shrinking over time through conversions and opportunistic repurchases.

Importantly, the capital stack has arguably improved since STRC launched. Strategy has increasingly shifted its funding mix away from heavier reliance on common equity issuance and toward preferred financing structures like STRC, while simultaneously reducing portions of the convertible stack through repurchases and conversions. The May 2026 repurchase of roughly $1.5B of 2029 converts is a good example of that broader trend: active liability management designed to simplify and strengthen the stack over time rather than simply expand it indefinitely.

That matters because critics often discuss STRC as though it sits beneath some static or deteriorating liability structure, when in reality the opposite has increasingly been true. The senior claims above STRC have become smaller, cheaper, longer duration, and more manageable relative to the underlying bitcoin asset base. Furthermore, Strategy has publicly stated intent to eliminate senior debt entirely.

None of this means the structure is riskless, as it still ultimately depends on bitcoin retaining long-term monetizable value. But being junior to a relatively small, cheap, staggered, actively managed debt stack is about as favorable as preferred subordination gets.

Myth #3: “It’s a classic Ponzi scheme.”

This is probably the most emotionally loaded critique, and it is also one where critics and bulls both tend to oversimplify things. The reflexivity is absolutely real, but that is not akin to a traditional Ponzi scheme.

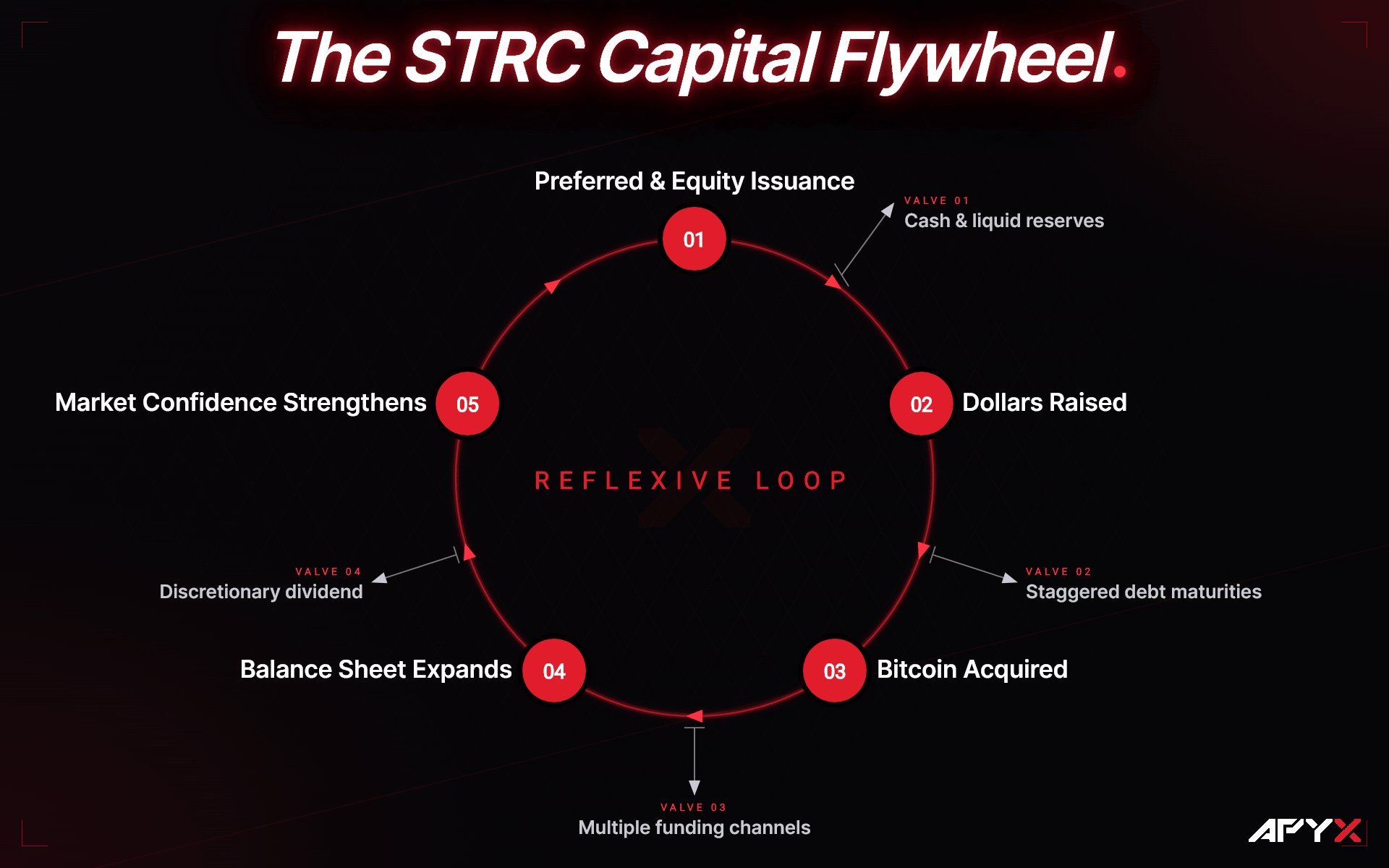

New issuance raises dollars, those dollars buy bitcoin, the larger bitcoin base supports the broader balance sheet, that balance sheet helps support confidence in the preferred structure, and continued confidence enables future issuance.

That flywheel exists and pretending otherwise immediately destroys credibility. But calling that structure a Ponzi fundamentally misunderstands what makes a Ponzi fraudulent in the first place.

A Ponzi is a fraudulent structure in which returns to existing participants are primarily funded by money from new participants rather than real underlying assets or productive cash flow, while relying on concealment, continuous inflows, and the illusion of stability to survive.

That is not what is happening with STRC. STRC issuance purchases a large, liquid, publicly disclosed asset sitting transparently on the balance sheet. The structure itself is openly disclosed in SEC filings and bitcoin sales are openly discussed. Furthermore, the reserve structure is visible and there is no hidden hole waiting to be discovered because the mechanism itself is not hidden.

The stronger version of the critique is narrower and more interesting: what happens if issuance slows materially? That is the real question. And the answer is not “instant collapse.” The structure was intentionally engineered with multiple pressure-release valves:

- Reserves,

- Staggered maturities,

- Multiple funding channels,

- And a discretionary dividend that can absorb stress without triggering immediate insolvency.

The wheel slowing is manageable. The wheel seizing requires multiple failures happening simultaneously:

- Severe bitcoin drawdown,

- Prolonged issuance freeze,

- Reserve exhaustion,

- And inability to use the discretionary dividend lever.

That is a real tail risk worth taking seriously, though it implies that one believes bitcoin’s day are numbered. But a highly reflexive capital structure is not automatically a Ponzi simply because it depends on confidence and continued access to markets - which is a phenomenon that exists for various asset classes and businesses.

Myth #4: “Strategy cannot actually cover the dividend.”

A lot of critics compare the preferred dividend obligation against Strategy’s software-business cash flow and conclude the coverage ratio looks weak or unsustainable. But that analysis applies the wrong framework entirely.

STRC was never structured as a claim on software cash flow. It is explicitly a bitcoin-linked balance sheet instrument. Judging it primarily through traditional operating earnings coverage is like evaluating an insurer solely by whether one quarter’s premiums cover every future claim. That is not how the structure is designed to function.

What actually matters here is asset coverage, and on that basis, the picture looks completely different:

- 843,738 BTC, worth roughly ~$65.3B ,

- Against approximately ~$6.7B of senior convertible debt post-buyback,

- And a broader preferred-plus-convert stack still covered multiple times over by the underlying bitcoin holdings.

The structure’s resilience comes from:

- Asset coverage,

- Liquidity,

- Reserves,

- Maturity profile,

- Funding flexibility.

Not from software operations independently generating enough cash to cover the coupon forever.

Critics sometimes respond by arguing that “the reserve and the risk are the same asset,” meaning bitcoin itself. That concern is directionally fair, but ultimately it just restates the underlying thesis exposure. If bitcoin permanently collapses as an asset class, the structure fails. That was always true, no amount of financial engineering changes it.

The real reachable concern is narrower: a severe cyclical drawdown coinciding with a prolonged issuance freeze. That is the actual stress scenario worth analyzing, not whether the software business alone can organically pay the dividend forever.

Myth #5: “STRC only works if MSTR trades at a premium.”

Some critics have attempted to derive precise “failure thresholds,” arguing that STRC enters a structurally negative-carry regime below roughly ~1.3x on Net Asset Value (mNAV). The issue is that many of these calculations incorrectly combine equity issuance accretion dynamics with fixed-cost preferred financing mechanics as though they are the same thing.

STRC is issued near par as a fixed-cost funding instrument. The economics are fundamentally different from selling common equity above Net Asset Value (NAV). That distinction invalidates many of the clean-looking “collapse threshold” calculations circulating online. But critics are still directionally right about something important.

While STRC itself is not directly gated by mNAV premiums, the broader accretion engine supporting the balance sheet absolutely benefits from common equity trading above NAV. During bitcoin drawdowns, those premiums naturally compress, which means the system becomes more reliant on reserves, bitcoin sales, and dividend flexibility precisely when markets become more stressed.

That linkage is real. What is overstated is the idea that there exists some precise mathematical cliff where the structure instantly flips from healthy to doomed. The dependency is indirect, slower-moving, and buffered by design.

Myth #6: “The dividend is discretionary, so they can just stop paying it.”

This is one of the strongest critiques because it identifies a genuine structural tension.

Yes, the dividend is discretionary and the reason it exists is because discretion materially improves solvency resilience. A structure able to defer a cumulative dividend without triggering immediate default or acceleration has far more flexibility during stressed periods than a traditional bond issuer facing the same cash shortfall.

But critics are also right that exercising that flexibility likely damages the peg. That is the tradeoff at the heart of the structure. The solvency protection exists precisely because the company can prioritize preserving the broader balance sheet over preserving near-term price stability.

However, there is another layer here critics often ignore entirely: the regulatory consequences of deferral. If Strategy were ever to stop paying the dividend, they would lose S-3 eligibility for approximately one year. That matters enormously because S-3 status is what allows Strategy to efficiently access capital markets through streamlined shelf registrations and rapid issuance programs. Losing that flexibility would materially impair the company’s ability to execute the very capital-formation strategy the broader structure depends on.

So the honest defense is not “they would never defer.” The honest defense is that Strategy itself has an overwhelming incentive not to. Their entire capital-formation model depends on STRC maintaining credibility and trading near par. The issuer has enormous incentive to preserve that confidence for as long as possible.

That does not make deferral impossible, but it makes it a genuine last resort.

Myth #7: “Raising the dividend from 9% to 11.5% is a distress signal.”

The bearish interpretation of Strategy raising the STRC dividend is rather obvious: an issuer repeatedly increasing its own funding cost to defend par can absolutely look like deteriorating credit quality.

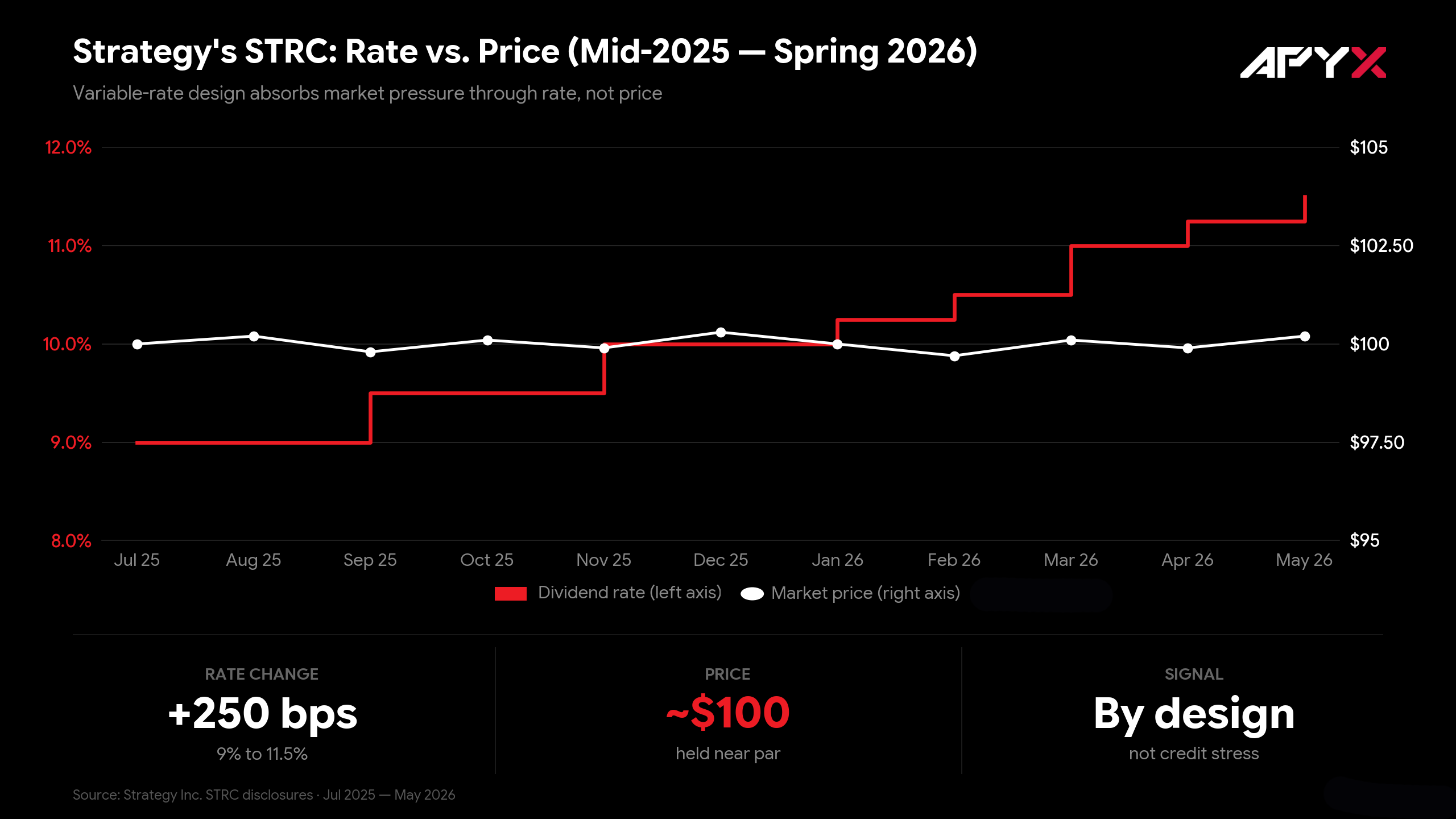

And to be fair, the repricing itself has been meaningful. STRC’s coupon increased from roughly ~9% at launch in mid-2025 to approximately ~11.5% by spring 2026, a ~250 basis point increase in under a year. That is not necessarily an irrational thing for critics to focus on.

The bullish interpretation, however, is that STRC was intentionally designed as a variable-rate instrument specifically so the rate, rather than the price, absorbs market pressure. Under this framework, the mechanism is functioning exactly as intended.

A fixed-rate preferred under similar conditions would likely defend itself through price declines instead of dynamic repricing. The interesting part is that STRC has generally remained near par while repricing, which matters. Genuine credit deterioration usually shows up as rising required yield and deteriorating price simultaneously, not one without the other.

That does not prove the bullish interpretation is correct, but it does make the “autopilot functioning as intended” explanation at least plausible. The more useful question is not whether the rate is rising. The useful question is, “Why?” Is the market repricing this specific issuer, or repricing the broader category? That is the actual debate.

Myth #8: “It’s a trap either way.”

The argument here is that holders lose regardless of what happens:

- If rates rise, credit quality is deteriorating;

- If rates fall, holders suffer capital losses.

This critique mostly confuses traders with long-duration income holders.

For leveraged traders or forced sellers, mark-to-market volatility matters enormously. For buy-and-hold income holders, it matters far less. A rate cut only creates realized losses if the holder actually exits the position.

And importantly, a rate cut itself would likely occur from a position of strength, where demand for STRC is sufficiently strong that the issuer can lower funding costs while preserving the peg. That is not a distress environment.

The “trap” primarily exists for traders, leveraged users, or forced sellers. It is far less relevant for the long-duration income holder the instrument was actually designed around and those allocating to STRC for the long-haul understand this.

Myth #9: “Tokenizing STRC creates a DeFi liquidation cascade.”

If tokenized STRC becomes heavily looped through DeFi lending systems, sufficiently violent funding-rate spikes can absolutely create reflexive deleveraging cascades. That risk is real, and importantly, it does not require bitcoin itself to collapse. But the mistake is treating this as uniquely an STRC problem.

This is a category-wide property of virtually any tokenized yield-bearing instrument interacting with leveraged secondary markets. The relevant differentiator between instruments is not immunity. It is redemption design, liquidity structure, and how effectively arbitrage mechanisms function during stress. Said differently, it's the protocols by which the leverage is built upon that dictates what, if any, a liquidation cascade could look like if it were possible.

Trying to fully dismiss this critique would be intellectually dishonest. However, here at Apyx, we’ve built the largest STRC-powered protocol with this risk in mind and have the relevant tools at our disposal to meaningfully reduce a systemic event occurring and having a ripple-effect.

Myth #10: “In a deep unwind, nobody actually buys.”

This is probably the strongest critique in the entire discussion because it ultimately reduces everything down to confidence: In a severe deleveraging event combined with a major bitcoin drawdown, who actually steps in to buy?

The bullish answer is value investors and the bearish answer is that sophisticated capital avoids catching falling knives.

Yes, the issuer can repurchase discounted securities accretively. Yes, long-duration holders may view discounts as opportunities. But both arguments quietly depend on the exact thing the critique is attacking in the first place: confidence that eventual recovery arrives.

This is the residual risk confidence-pegged systems always carry and the honest move here is not to manufacture some airtight rebuttal that does not actually survive scrutiny. The honest move is simply to acknowledge the limit.

Par restoration ultimately depends on confidence, not contract. That is true here, and it is true across virtually every confidence-defended financial structure. Said differently, this is not a risk or a critique unique to STRC.

Myth #11: “It isn’t actually bitcoin-backed.”

This critique exploits the gap between economic language and legal language. Legally, STRC holders do not possess:

- A lien,

- Direct collateral rights,

- Or claims on specific bitcoin.

That is true and should be stated plainly. But critics often overextend that clarification into claiming the structure is therefore “unbacked,” which does not really follow.

In financial language, “backed” frequently refers to economic exposure to an asset-rich balance sheet rather than segregated pledged collateral. Most unsecured corporate claims work exactly this way. So the honest framing is straightforward:

- STRC is unsecured,

- Holders do not own pledged bitcoin collateral,

- But the economic backing from a large disclosed bitcoin balance sheet is still real.

The clarification matters and the accusation of unique deception usually does not.

Myth #12: “The tax treatment only works if Strategy never becomes profitable.”

This critique is directionally correct, but often overstated. The favorable return-of-capital treatment is real today and materially beneficial for holders. That is not hypothetical, it is the current tax treatment.

At the same time, the favorable classification is genuinely linked to the company’s earnings-and-profits posture. That dependency should be stated openly rather than hidden. The honest framing is simple:

- The tax advantage is real,

- It appears durable under current guidance,

- But it is not guaranteed permanently under every future scenario.

A sophisticated holder should understand both facts simultaneously.

Final Thoughts

The most important thing to understand about STRC is that it is neither a riskless income instrument nor some obviously fraudulent structure held together by accounting tricks. It is a highly reflexive, confidence-dependent, bitcoin-linked perpetual income structure engineered around long-duration resilience.

The strongest critiques are not the simplistic ones, they're the ones that identify where confidence matters more than contract, where capital access matters more than operating cash flow, and where cyclical volatility can become self-reinforcing under stress. But many of the loudest criticisms still overstate their conclusions.

STRC is not secretly riskless. It is also not secretly misunderstood junk destined for inevitable collapse. It is simply a leveraged long-duration bitcoin capital structure whose resilience ultimately depends on whether bitcoin itself remains monetizable collateral over the long run. That is the real debate.